Company Update: Yangzijiang Financial

Share buyback, Increase in Dividend

It is always amusing that when management tries to influence the share price through a capital allocation exercise.

It looks just like parents trying to influence their kids decision, it usually does not work in the short term.

YZJ Financial’s management has been throwing everything they have to rouse the share price and I still think it will not work on the short run.

It may just work in 1 year time…

6th May 2022:

YZJ Financial is going to do a 10% share buyback

Since the share buyback had been announced before the de-merger exercise, that is a non-news.

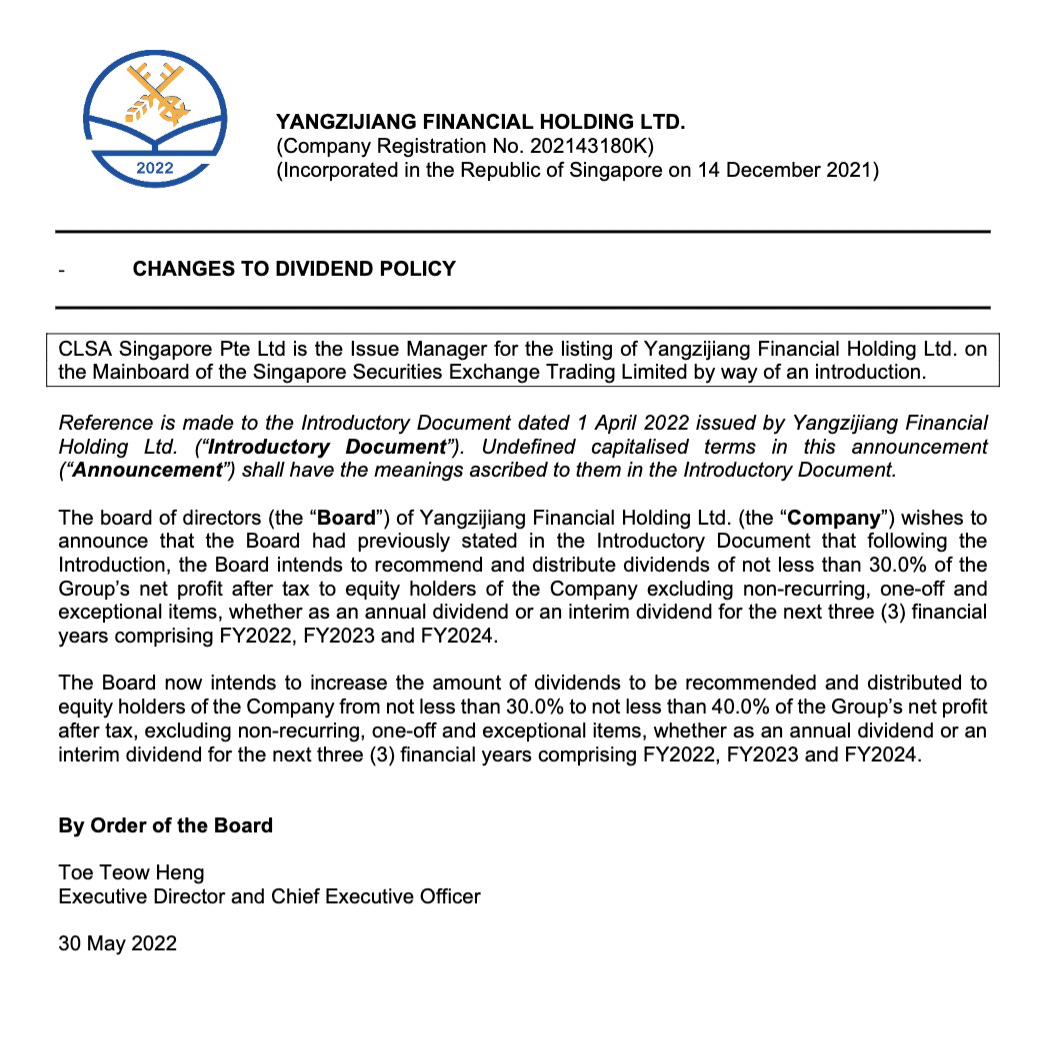

30th May 2022:

YZJ Financial is going to up their dividend policy from 30% to 40% for FY2022 - FY 2024.

The change in dividend policy is a new news to the market and my guess is that it will mean different things to different type of investors.

Institutional Investors:

For the institutional investors who are still trying to get out, the new news of higher dividends are non-news to their ears.

They just want OUT!

No institutional investors would want to be involve in investing in debt instruments in China when Zero-Covid policy rages on, President Xi is still president and the possibility of China-Taiwan war .

They are just glad that they can get out at higher prices than a week ago.

Retail Investors (yet to sell):

For the retail shareholders who has yet to sell, they would finally be convinced to keep their shares?

Would they be buying more shares?

I doubt so…

They will be conservative and wait for the dividend announcement and possibly declare victory from that.

Retail Investors (yet to buy):

For the retail shareholders who are looking for dividend, would they be convinced to buy NOW?

I also doubt so.

Most of them would be unsure what the dollar amount for 40% dividend payout is.

Since they are clueless, most will refrain from doing anything.

Slightly Enterprising Investors:

For the slightly enterprising investors, it could be interesting to try to estimate the weighted returns.

The good news is that the dividend can be estimated.

With a NAV of around SGD 1.001 per share, and an ROE of +/- 10%, the earnings per share would be around +/- SGD 0.10.

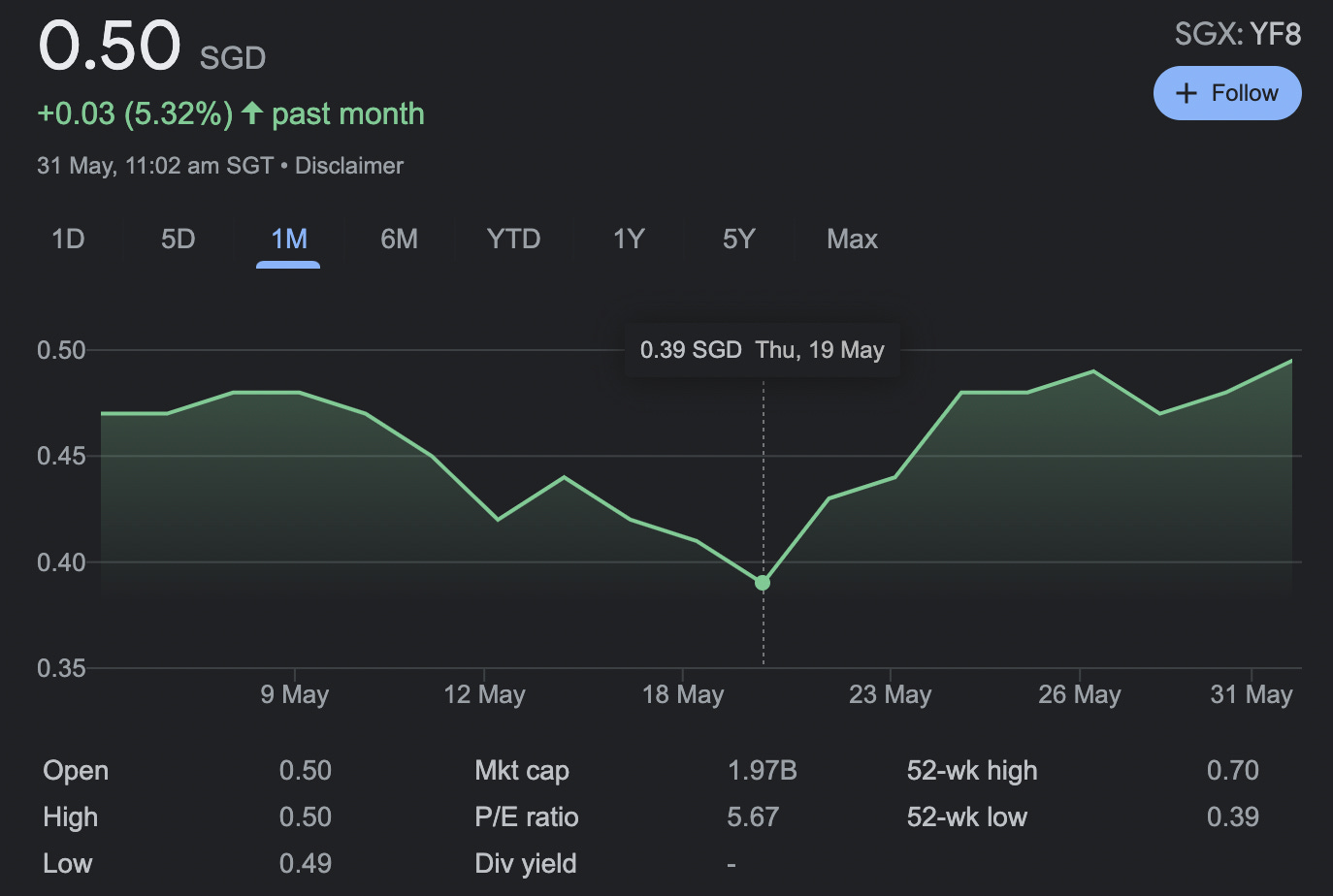

If they pay out 40%, that would imply a dividend of +/- SGD 0.04 and at current share price of SGD 0.50 would imply a 8% yield.

Since a 5% yield looks about fair, the fair value for the shares would be SGD0.802?

If YZJ Financial trades up to SGD 0.80, that would imply a 60% increase in share price in 1 year time?

What about the downside?

With institutional investors more or less cleared out, the avalanche of sell orders should slow down soon?

Share buybacks should commence if the share price remains at this level.

The downside looks really minimal at this point onwards

Ending in a similar fashion to how I ended last article on YZJ Financial.

Welcome to the world of passive enterprising investing where the patient enterprising profit from the passive clueless!

Depend on the exchange rate of RMB/SGD

4 cents divide by 5% = 80 cents