2024 Week 31

YesAsia, Chicmax, Hang Lung Properties, Activation, Powermatic

Writing period: 30th July 2024 - 5th August

YesAsia - the market knew…

In week 16, i commented that “it is always wise to get out when the valuation is far removed from the current realities of the business”. It seems that the market is correct is getting excited.

Now we know why the market got so excited last month. After the news, the stock continued to make new high at HKD 5.51 before retreating to HKD 3.64.

If it falls a bit more, this may once get attractive enough to get back into my portfolio. If a distributor is not up your alley, what about a branded cosmetic company?

Chicmax - the market derated…

While the American and the European are still at K-Beauty, Asian has moved on to C-Beauty. It seems that women can see more shades of colours than men and thus they have insatiable appetite for cosmetics?

Chicmax is going to draw in > RMB 800m in net profit. Valued at HKD 13,490m, Chicmax is closing down to PE of 15x with a 24% roe. This is starting to look like a bargain?

The worry is that the growth KANS is a one off and would taper off soon. If I own a C-Beauty brand, I will be copying what the K-Beauty is doing to expand throughout the world.

Slap on some english instruction, get some “asian international” stars to endorse their product and then sell them through beauty multi-brand retailers, like Sephora, Ulta and online on Amazon and YesAsia, and proprietary official websites.

Watch out for the onslaught of C-Beauty soon!

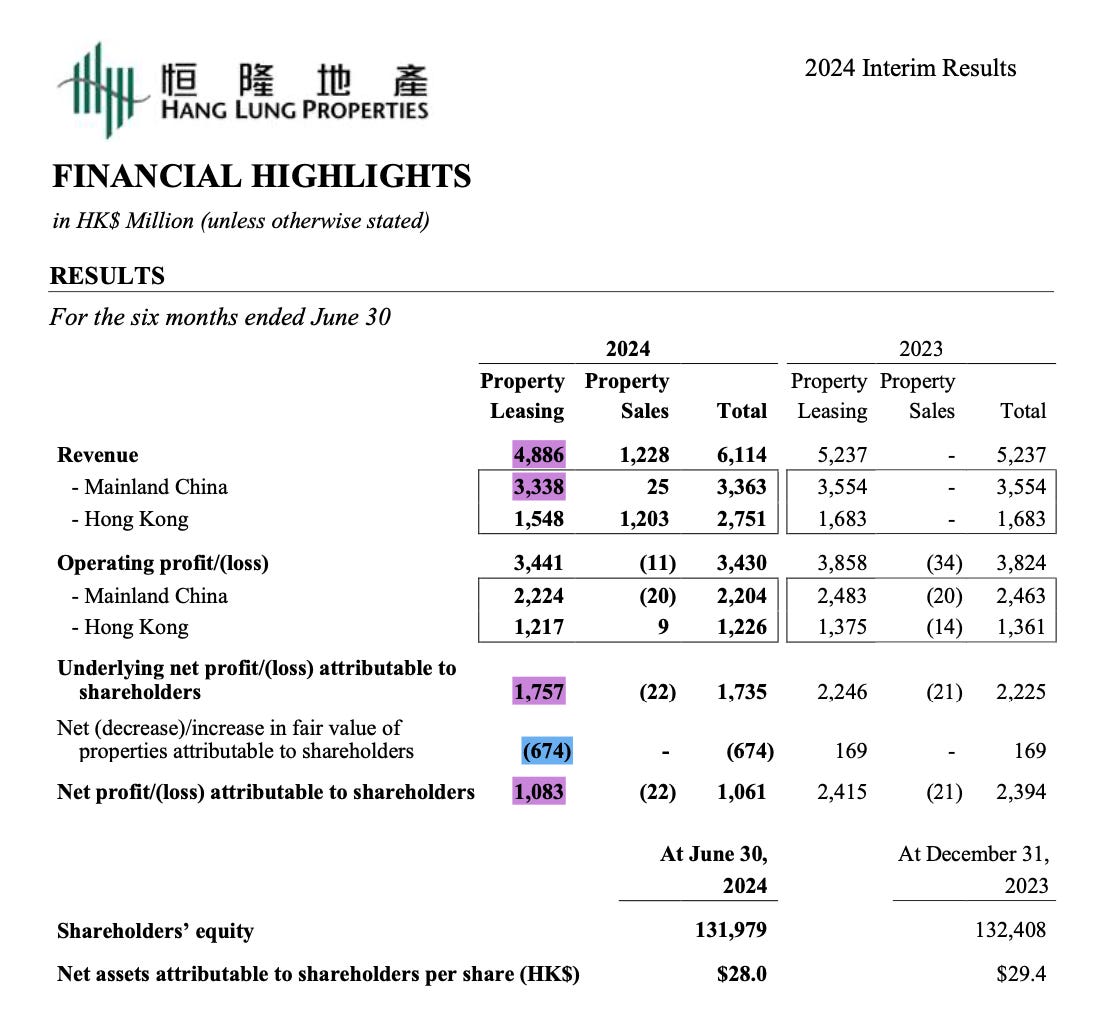

Hang Lung Properties - the market got disappointed

If you are looking at getting the best retail assets in China, then Hang Lung should be the preeminent choice.

If what the media is saying is correct, then all the Chinese are going over to Japan to buy luxury goods.

Maybe the recent yen increase would put a stop to that?

In the short term, it seems that Chinese luxury retail will continue to shrink…

I keep a look out for Hang Lung not because i am into property but because I am vested in the Chinese luxury retail spending through Activation.

The good news for Activation is that the luxury marketing spend is base on the passport spend and not on country spend. So it does not matter if the Chinese spend in Japan or Europe.

The bad news is that luxury spend is definitely going to be lower for the next few years?

If I want to bet on the Chinese buying more luxury goods in 5-10 years time, maybe Hang Lung Properties may be a surer bet?

I am sure the shopping malls will still be around but would Activation still be the top player in the luxury marketing space in 5 years time?

Far Ltd - the market continues to not react…

No significant new news here since 11th June update except for “First cargo was loaded and ramp are expected to continue through 2024”

But alas, with the oil prices dropping below USD 80… it seems that the potential monetisation will become smaller?

Now the potential buyers will have less margin of safety in term of the oil prices but at least we have another USD 3-7 to go before it drop below USD 70…

I guess that why there is never a sure thing on the financial market…

Powermatic - where the market react to a shareholder friendly management…

One of my investing buddy wrote an article and posted it on nextinsight.

The gist of the story is that the management has been listening to shareholders and has turned increasingly shareholder friendly through the years.

Anyone who has been to PMD’s shareholder meetings (especially in recent years) could easily see that its directors are fully engaged and were fully able to express their voice in response to questions from shareholders.

The commitment to create value and distribute excess capital to reward ALL shareholders is especially commendable. -Free Wifi

That continued work on niche business and the continued monetisation of hidden assets meant that Powermatic would have returned a 1,116.4% return over 19.25 years.

Since most of us are not that patient to wait for 10 - 19.25 years, I guess that we have to contented with whatever gain that could be realised - when Powermatic complete the sale of their Harrison Food Factory and proceed to distribute out the excess cash on their balance sheet…

I have scheduled a meeting with Pentamaster’s management in Penang, Malaysia on the 14th August 2024 morning to understand more about their newest development.

If anyone want to tag along for the meeting, just drop me a DM.

Yes, pls do share your penta visit. so far disappointed with their performance given that there is a major semi build up in malaysia. they should consider share buy back as it's severely under valued. also need to up the div payout(to nearer 30-40%) so that long term investor gets paid for the wait to growth.

Please do share your findings with the Penta management on future substack posts, if possible!