2024 Week 22

Mermaid Maritime, Semler Scientific, Far Limited, China Trip

Mermaid Maritime - it is just a blip:

Since posting about Mermaid’s pullback in price from SGD0.16 to SGD0.13 on 2024 Week 20, the stock price has continued to power up.

With a market capitalisation of SGD 251m, it is hard to justify that Mermaid is a value stock. At a higher price, it is getting harder to justify holding a full position. Depending on your horizon, it may make sense to start trimming the position.

It is more of a momentum play now. The main trade is that growth is going to continue and the margins are going to hold up.

Since Subsea work typically comes after the discovery of oil through an oil rig, my guess is that the subsea sector up-cycle is just coming.

If you pull out the chart to the max, the recent rally is just a blip in the Oil and Gas services sector turnaround and recovery.

Semler Scientific - Taking the LUCK”Y” bitcoin:

Imagine you see this after just taking an initial stake in the company and they release this piece of news.

I always thought that treasury are meant to

provide a safety net

preserve bullets so that one can pounce on an opportunity

for the company.

Somehow I cannot see bitcoin serving either of the above mentioned functions.

The stock price looks like this right after the news.

The management manages to get the adrenaline and the testosterone pumping and I am thanking my lucky star and saying adieu to this position.

FAR Limited - not how much but when?

FAR Limited operates as an oil and gas exploration and development company with primary assets in West Africa and Australia. The company holds a portfolio of exploration licenses in the Gambia and Guinea-Bissau.

-Tikr.com

But FAR is no longer

oil and gas exploration and development company

has any asset in Gambia or Guinea-Bissau

Currently, FAR only holds a Contingent Payment from Woodside for the Sangomar field which is expected to commence its first production in mid-2024 which is like now?

It is also the intention for FAR to monetise their contingent payment to get the money NOW than in December 2027.

So FAR is going to receive USD 55m/ AUD 82m in 2027 (around 3.5 years time) or an early contingent payment of around USD 30m / AUD 44m (depending on the discount rate you are using).

So you either get USD 55m/ AUD 82m in 2027 which is not a bad outcome since you basically double your money in 3.5 years (which should be around 23% per year) or you get a payout north of AUD 44m soon.

I like the odds of not losing money here.

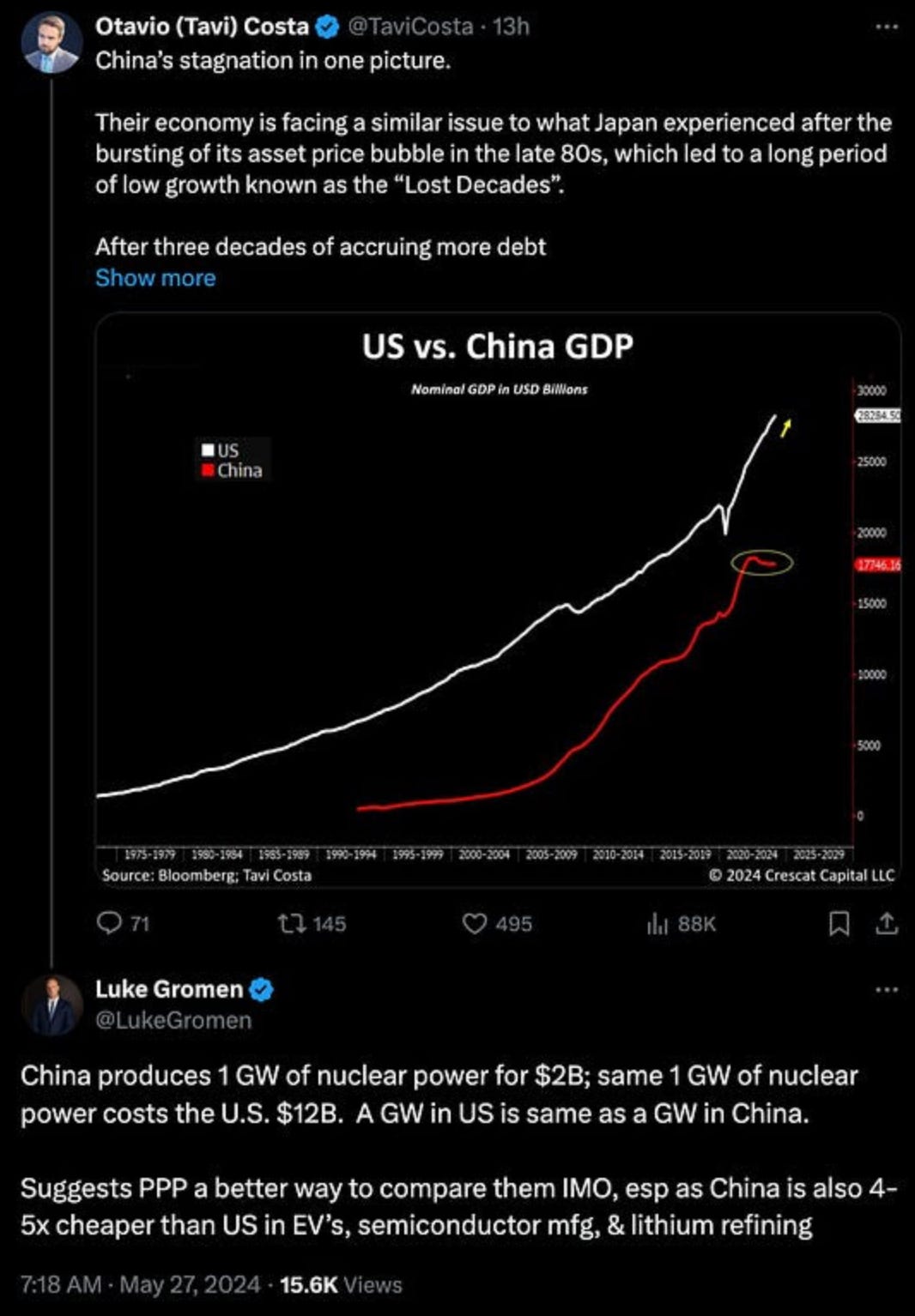

China - If there is one metric to tell it all…

I know I am supposed to

Trust but Verify

- Ronald Reagan

Sometimes the concept below just simply appeal to me.

If there is one metric that helps to determine the competitive advantage of a nation, it has to be the cost of generating power (and the amount it could generate at that price).

Judging from Luke Gromen’s comment, China is gaining a significant advantage against the US unless something dramatic happens on the technological front for energy.

I believe the China bull market or turnaround is only starting.

There is still time to get on the train.

I am flying once again to do some research, first to Hong Kong, Shenzhen and then Beijing.

Have fun on your trip, looking forward to hearing what you find