More purchase on the Chinese Covid recovery...

and some review on our previous picks

Written on 10th April 2023

When the Covid recovery in China and the expectation that Chinese would travel the world and buy tons of luxury, which sector will recover next?

Since everyone is back in the streets, having meals and choking on fish bones, I am sure someone somewhere in China will need medicine for eye injuries, dry eyes, refractive and cataract surgery, maybe some sprays and powders to treat repairs and regenerates cells damaged by bruises, burns, contusions, cuts, surgery incisions, skin grafts, skin resurfacing, laser therapy wounds, bedsores, fistulas, and cervical erosions.

HISTORY RHYMES…

On 17th May 2021, when China is the envy of the world for normalising life by closing to the world, this is what happen to their sales.

Essex Bio-Technology (Essex) share price spike from HKD5.24 to HKD7.83 before COVID cases started to inch up in China and the share price went into a free fall again.

With COVID effectively “over” in China now (2023) and with most hospitals getting back into their normal routine, would the stock price do what it did last last Summer May?

Essex Introduction:

Essex is primarily made up of the ophthalmology and surgical (wound care and healing). The core products that are under each segment are:

Ophthalmology – Beifushu series (Beifushu eye drops, Beifushu eye gel and Beifushu unit-dose eye drops), Tobramycin Eye Drops, Levofloxacin Eye Drops, Sodium Hyaluronate Eye Drops and 適麗順® (Iodized Lecithin Capsules)

Surgical (wound care and healing) – Beifuji series (Beifuji spray, Beifuji lyophilised powder and Beifuxin gel), Carisolv® dental caries removal gel, 伢典醫生 (Dr. YaDian) mouth wash and 伊血安顆粒 (Yi Xue An Granules).

The turnover of Ophthalmology and Surgical is approximately 42.0% and 58.0% of the Group’s turnover respectively.

The defensibility of their product comes from the patent, the low price they are willing to sell at and their wide distribution network.

Currently, they have 2 promising drugs in the pipeline SkQ1 with Miotech which treats the dry eye disease and anti-VGEF a biosimilar with Henlius which treats Wet-AMD.

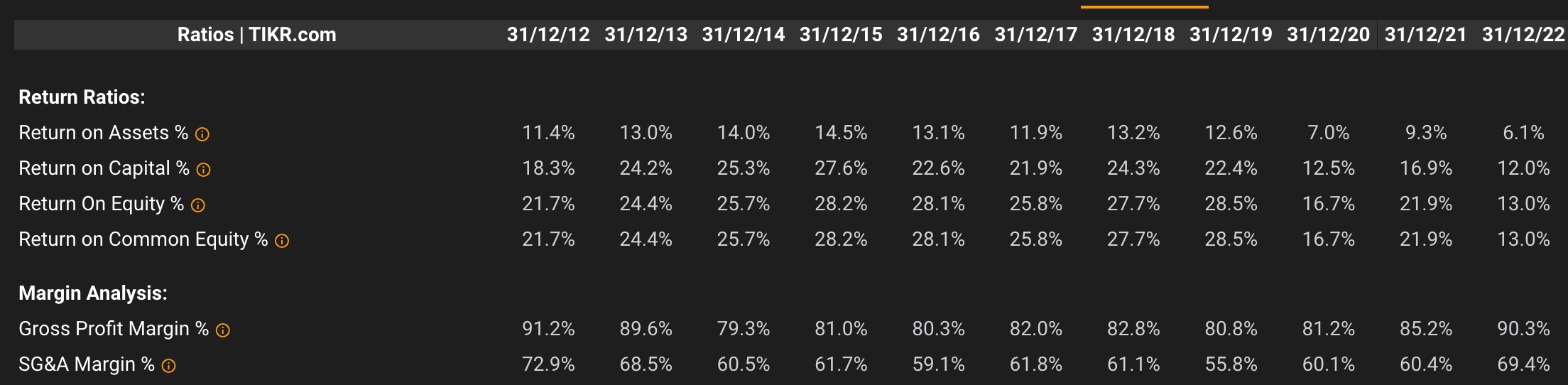

VALUATION:

If the assumption is a normalisation of earnings for 2023, then net profit should be around HKD302m (2019) and HKD345m (2021). Taking a median of these two number, we will get an estimate of HKD323.5m meaning that Essex trade at 6.6x PE.

Should Essex should trade at 6.6x normalised PE?

This is a company that has consistently average more than 20% in ROE every year except the 2 Covid years of 2019 and 2022.

Maybe there is more than meet the eye for this low PE?

GOODWILL & INTANGIBLES:

The biggest item on their balance sheet is the goodwill and intangibles.

I am going to focus solely on the intangibles.

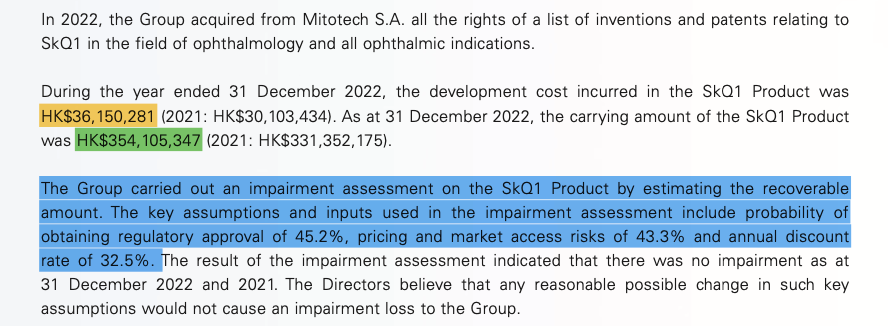

The intangibles consist mainly of development cost for SkQ1 with Miotech (HKD 354m), anti-VGEF with Henlius (HKD 215m) and Iodized Lecithin Capsules (HKD144m).

For SkQ1, Essex seems to be conservative in their valuation model.

For anti-VGEF, Essex did not mention the regulatory approval and market access risk. I think that is reasonable since this is a biosimilar with low hurdle.

If any of these programme fails, there would be a substantial write down in intangible.

In addition HKD278m is not being accounted for here and it may be the case that Essex has been “over earning” for the past few years. Being conservative, it may be prudent to adjust the past and current profit down for these unaccounted intangibles.

If this is any assurance, I do not think any significant write down will happen within the next 2 years.

PATENT:

Their patent for this will end in 2030.

Up to the date of this report, a total of nine patents have been granted to the Group, out of which seven are innovation patents(發明專利)on the application of bFGF. These seven innovation patents will enable protection of our existing Beifuji and Beifushu series of products till 2030.

-2013 Annual Report

So the patent cliff is coming and there is no new drugs from Essex YET. They have another 6 years to go and maybe you should only pay less than 6x PE for this company?

For that we are assuming that nothing good comes out from their R&D programmes. Their new drugs tackling dry eyes with Mitotech and wet AMD with Henlius looks promising and the hurdle for each to get approve does not seems that high.

On a side note, I expect Essex to continue dominating their category of drugs even when their patent expires. They are already providing the medicine at the lower range of their competitors’ pricing and I cannot see how they will start losing market shares when the drug goes off patent.

MANAGEMENT:

Patrick Ngiam. He seems to be pretty successful businessman but he does have a litany of destruction at his feet too.

Some companies which he has involved directly or indirectly with include,

IPC Limited (Chairman & Chief Executive Officer) which is a shadow of its previous self.

Wilton Resources (Non-Executive Director) which is down 84% since 2014.

Asiatravel (Non-Executive Director) which has since been delisted.

But how many businessman comes with zero failure?

INVESTMENT (CONVERTIBLE LOANS):

Essex do have a habit of dabbling in convertible loans to small companies. There are some hits and misses. These the the hit and misses from FY2022 annual report.

Investee A:

The interest is pretty low. If investee A is unable to repay, then we could effectively write off the company? Definitely a miss.

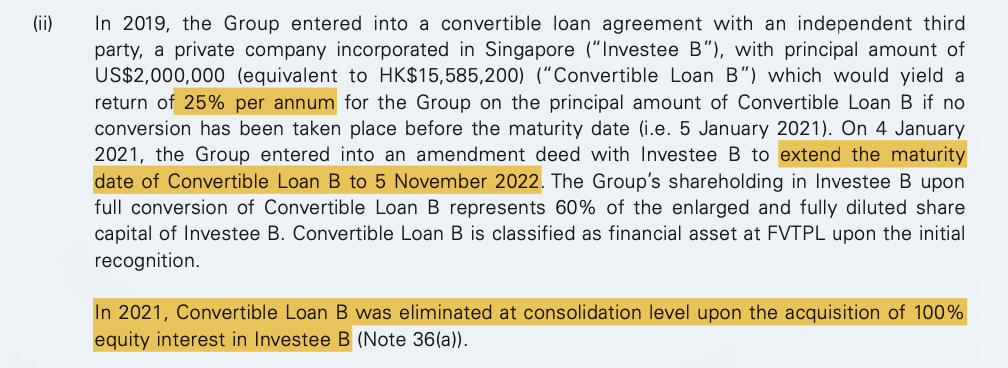

Investee B:

This look like a miss too. Investee B took up a convertible loan at 25%! That means that they are on the verge of dying. The elimination of the convertible loan in 2021 is ….

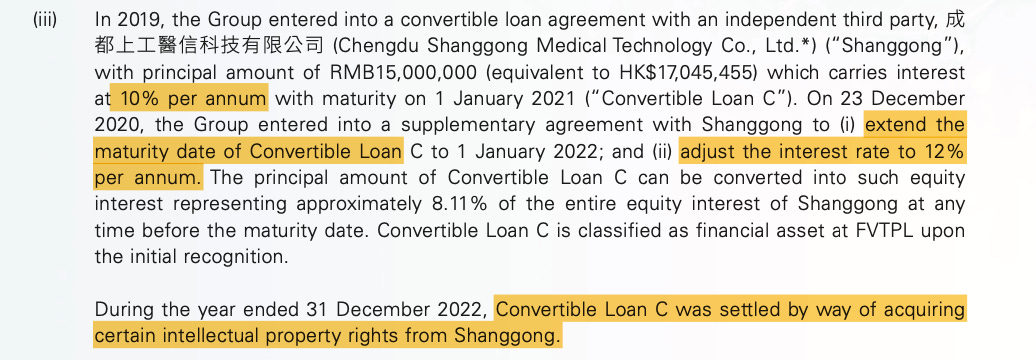

Investee C: Chendu Shanggong Medical Technology

I don’t know what to make of this. They managed to take Iodized Lecithin Capsules from them and I guess you can call that a hit.

Investee D: Antikor Biopharma

This is still a work in progress.

Investee E: Mitotech S.A.

I could call that a win? Since Miotech “gave” Essex SkQ1 which is one of the 2 drugs which will form the backbone of their future development.

So out of the 5, we have 2 possible hits, 2 possible misses and 1 meh for FY2021/2022… If you look back into history, it has been a mixed bag of acquisitions and divestments… so make your own conclusion of this business strategy of using convertible loans to get stake or drugs from promising companies…

LOANS (CONVERTIBLE LOANS):

This stands at HKD 157m. Since the conversion is at HKD 5.90, the chance of conversion is pretty low now.

Overall:

There are potential issues with Essex (like the large goodwill and intangibles, 7 years to the end of patent, the myriad of convertibles loans given and received but these problems will not be immediately evident (at least not in the next 2 years?).

What I am also pretty sure of is that eye and skin injuries will be on the rise in China since everyone is no longer staying at home.

In addition, any optionality of good news from either of the 2 potential drugs could only be good news for the company.

This is a bet and I have started building a position on Essex 1061.HK with an average price of HKD3.84.

Do your own research and I may buy and sell the above mentioned stocks at any time.