Temasek is investing in Zomato

And we think there is a chance it will turn into rotten tomato!

For subscriber who had previously signed up to us after our rant on Temasek, we continue to think they are doing a bad job. Temasek is not thinking across public and private investment like they should. Sometimes, it is just better to buy public when it is cheaper.

Indian food delivery startup Zomato has raised a $62 million financing round from Temasek Holdings unit MacRitchie Investments, which is an existing investor in the food delivery service. The round values Zomato at about $3 billion.

Also in India this week, Dunzo, a startup that delivers everything from restaurant meals to groceries to household supplies, announced it had raised $28 million.

So the food delivery business in India is going to be bloody! Remind us of the whole co-working space craze previously. We are never big fans of the food delivery space, but if we can get it for free, we do not mind the investment.

Below is the set of old article on the thesis on Prosus. Maybe Temasek should just buy Prosus. It is a cheaper way to play the venture capital game. But heck, the guys at Temasek will never admit their initial mistake… Maybe they also need to support the ever rising valuation like what Softbank did until it went kaput…

Do subscribe to our service if you are keen to receive our monthly newsletter!

Buying start-ups at a discount on the stock exchange:

Written: 8th May 2020

The startup space is exhilarating, deals done with gut feel about the business, about the founders, about the possibilities of global domination and riches. While start-ups often fail even at later funding stages, sometimes it is possible to do some startup investing on the stock market.

There is a few possible ways to do so.

These include:

Buying a bunch of more mature startups (Mature) which were listed on the junior exchanges

Listed Venture Capital (VCs) companies

Listed companies acting as acquirers and consolidators (Acquirer)of a particular vertical

Listed traditional companies (Old) trying to find growth by investing in the startup space

Option 1 (Mature) is usually best avoided as they are no different from investing in an early stage startup. Once a while you may hit an Amazon or Google but I have no particular edge in picking an Amazon out of the many Pets.com.

Option 2 (VCs) is not so ideal as they are taking shareholder money to invest when they should be using their LP's money. A good VC or fund manager do not have a lot of good reason to list their companies...

Option 3 (Acquirer) is mildly interesting as we could understand what the company is aiming to do and can do by having a good understanding on the value of their acquisition and consolidation exercise. If successful, the "Acquirer" is usually highly valued as the investing community is expecting high revenue growth from them.

Option 4 (Old) shows that the company is willing to look at new ways of doing things. While they usually have a profitable line of business and is looking to tap on startups to extend their reach, the chance of succeeding in early stage start-up investing is still very low. The only risk mitigating factor is that the "Old" has the knowledge of the industry to possibly scale the start-up. "Old" is also usually viewed as investment holding companies with no focus and direction. And often they are sold at a discount to their book value.

What if we can get 3 + 4 with a Spinoff ?

Then we will be getting a Growth Firm priced like a value stock.

The company that I am talking about holds a substantial stake in Tencent. In addition, they are into the business of

Classified

Payment

Food deliveries in the fastest growing regions of the world!

The company is Prosus, the spinoff company from Nasper.

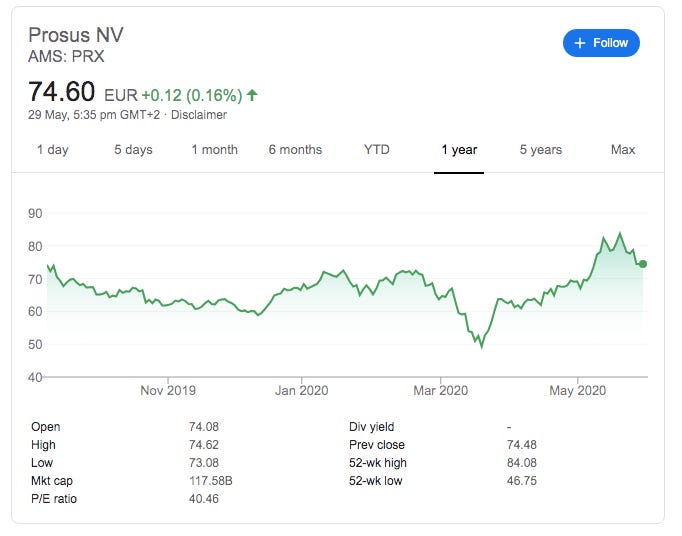

In term of market capitalisation, Prosus is the second largest technology firm in Europe after SAP. In addition, their whole capitalisation can be accounted for by their stake in Tencent. By buying Prosus, we get the 1. Classified, 2.Payment and 3. Food delivery companies for free!

Let's delve a little bit deeper into their assets they own.

Balance Sheet:

Quoting (below) from the 20202Q financial statement. They have sufficient net cash balance of USD5.4b. That seems like a fine balance sheet!

We had a strong net cash position of US$5.4bn. This comprises US$8.7bn of cash and cash equivalents (including short-term cash investments) and primarily reflects proceeds retained from the Flipkart disposal and sale of Tencent shares in the 2018 financial year. We had US $3.2bn of interest-bearing debt, excluding capitalised leases. This resulted in net interest income of US$16m.

Listed Assets:

Prosus owns around 31% of Tencent. Since Tencent is valued at around HKD 4 trillion = EUR 463,384 million (m) in market capitalisation, their 31% stake would be worth around Eur 143,649m. We are paying Eur 117,580m to get value of Eur 143,649m. That is interesting but not enough, let see further on what other easily identifiable assets that Prosus owns.

Prosus also own a suite of other listed companies such as

28% of mail.ru

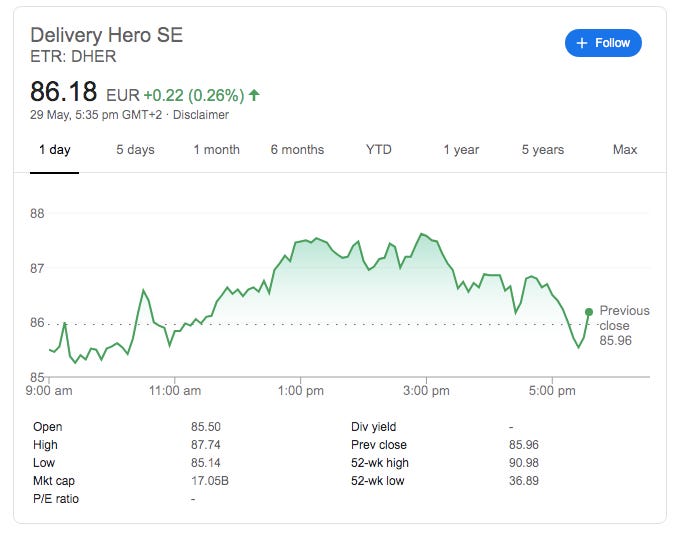

22% of Deliveryhero (leader in 34 of 41 markets they are in)

5% of trip.com

While getting Tencent at current market price, we will get the rest of these listed companies for free as well. You can do your own calculation below. While these "spare change" does not make much of a dent on Prosus valuation, they provided a much needed additional margin of safety to this valuation exercise.

Like a well stocked candy basket, Prosus do have a few more nice candies which could provide a good kicker to Prosus valuation exercise.

Classified Segment:

In the classified segment they own OLX Group. This group of classified businesses are the leaders (29 out of 30) in the market they operate in. They have over 300m users and best of all they are profitable as a whole. The classified segment make around USD37m in trading profit. If they are to list the classified business as a whole, the conservative valuation would around at 1x sales which is around USD1 billion in dollars. For the Singaporean reader, you may be glad to know that Prosus also owns around 12% of Carousell.

Payment & Fintech:

Payment and Fintech is a segment which we are very excited on. Their core brand PayU are behind Paytm and Google Pay. The average daily transaction in India increased by 39% for 20201H. Paytm processed a lot more transaction constituting 50% of the market shares. Interestingly Paytm gross transaction value per transaction is much smaller in value than PayU. On the long run, we would expect the guys with the higher transaction volume to win the game. But on the short run, the company - PayU which has higher gross transaction value will turn in the better financial. The simple solution is that PayU could go on a shopping spree to buy smaller players like RazorPay to consolidate the market. Or if the India government allows, allow Paytm to buy PayU to create a payment behemoth in India.

Food Delivery:

This is the segment which we are least interested in. The reason is that we do not like to order in. It goes against our grain of supporting good food and having a meditative experience. We also do not like the waste created by the delivery companies. But nevertheless, human are lazy by nature and what is better than having food delivered right to your bed, opps not bed but doorstep.

The food delivery businesses are leader in 36 different market. Their brands include

Delivery Hero

iFood (Leader in Brazil)

Swiggy (Leader in India)

With the Covid-19, we could not deny that it is possible that food delivery business is one industry that has been bolstered by this crisis. Take a look at the food delivery business by thinknum.com. You will start to realise that food delivery is a global operation now. While iFood and Swiggy is not within the map below, they will be nice addition to players like UberEats and Just Eat. Or the easy way out is that Prosus could swap out stake for iFood and Swiggy for a substantial stake in Delivery Hero (Delivery hero owns the FoodPanda brand).

Conclusion:

Out of the many bets that Prosus had made, one or two may turn out to be like Tencent is to Nasper. While a lot of the analyst hated the concept that Prosus seems to be throwing mud at the wall and seeing what sticks. Prosus's throwing of the mud seems well executed and the chance of them sticking should be higher (than OURS).

And best of all Prosus is under-weighted on most European index funds. It is weighted based on its free-trading shares (not owned by Naspers), not the entire value of the company. As Nasper continue to sell more Prosus share and do buyback on their own shares and thus make more shares available, it may actually boost Prosus' weighting in these indexes.

And if we are really lucky, in September 2020 when Stoxx rebalance, there is a chance for Prosus to be included in the index. If that happens, the the passive money will be helping us to carry the price higher irrespective of what Prosus does till then.

Buying food-delivery company at a discount on the stock exchange:

Written: 11th June 2020

Just Eat Takeaway.com, the largest Amsterdam based food delivery company just announced that they are buying over Grubhub in an all stock deal valued at $7.3 billion. The combined company would have a major presence in four markets, the US, the United Kingdom, the Netherlands and Germany.

Just Eat stepped right in after Grubhub deal with Uber Eats ended. With this consolidation exercise going on, we wonder how Prosus will benefit.

Prosus food delivery businesses are leader in 36 different market. Their brands include

Delivery Hero

iFood (Leader in Brazil)

Swiggy (Leader in India)

Now we can imagine that it is almost time for the game of worldwide domination. Prosus stake in Delivery Hero could determine if Uber get a foot in Europe, while iFood and Swiggy being leaders in their respective country are important markets for expansion by any global food delivery company.

Or maybe this food delivery consolidation exercise will not go global as venture capital money are scarce.

Or maybe, the focus of the entrepreneurs are to look at their market and try to turn profitable.

While we may never know how things will turn out, do remember that at current price, we are paying nothing for the food delivery companies residing in Prosus portfolio!

Prosus Annual Results - 31 March 2020:

Written: 22nd July 2020

The thesis remains intact!

Prosus still trade below the valuation of their 31% in Tencent. With the general consensus remains that Prosus valuation discount to its investment will no longer shrink and upside is minimal while we continue to believe otherwise. You do not buy a tech holding company for its defensibility, you buy it for its ability to

invest intelligently and consolidate various verticals.

transform their illiquid investment into liquid assets through the sale of a division either receiving cash or shares in a listed entity or a listing of a division.

provide good capital allocation between cash, debt and equity financing.

Prosus has been all the above and should be able to realise more value as their main segment such as classified and food delivery matures.

There is early indication that Prosus is the frontrunner for eBay classified assets which will cost Prosus around USD$8b. The bulking up of classified will enable Prosus to start the spinoff of their classified division into a separate company further highlighting the value of a large diversified classified division.*

The revenue growth and the M&A of the food delivery business continues and should drive margin expansion. There is a good chance for Prosus to sell their Food Delivery business into a listed entity receiving cash/equity in return.

PayU will be acquired by a larger entity who do not wished to build spend time acquiring the requisite licenses in Asia.

Optional: If we are really lucky, Prosus may be included in the Stoxx 50 in September 2020 which will further increase the demand of Prosus shares.

The above will help to raise Prosus intrinsic value and they are not hard to do in this environment.

The market will finally understand how to value Prosus using Tencent, Mail.ru, Classified, Food Delivery and Payment and Fintech, with a conglomerate discount of 20% - 40%. As long as market is able to recognise the sum of the parts, we will be richly rewarded even with a conglomerate discount factored in.

Average Purchase Price: EUR 73.21

Disclosure: At the time of publishing Wee Hiang has a position in the above company. Holdings are subject to change at any time. This report, and disclosure, should not be considered to be a recommendation.

*Adevinta won the deal to acquire eBay's classified in a $9.2b deal. Prosus share price rallied as a result. The market seems to like cash more than eBay's classified.