Special Situation Portfolio #1 DXC Technology

Digitalisation of the economy

Do take note that the pricing of the counter have moved up substantially from our average entry price of USD 16.903. We started buying at USD 15.2 and had been buying all the way up to USD 20.22.

We are hopeful that the transformation is happening right now!

We have an position in this constituting around 4% of our portfolio and we plan to bring it down closer to our ideal 10% as more data come in.

This position forms part of our Special Situation portfolio.

While we believe in the Asian story, the African story but we cannot deny or ignore the American story. US remains one of the most dynamic enterprise creator in the world with Alphabet, Apple, Amazon. Damn, we need to buying companies starting with A. There seem to be some correlation here.

Another trend is the continued digitalisation of the economy. We are zooming from home, chatting to chatbots on the screen… You got the drift.

But everything related to the internet is getting so expensive.

Maybe outsourcing? That is such a passé term and that is where we start for this article. For those who are uninitiated, outsourcing is still well and alive. While most people idea of outsourcing starts with the concept of outsourcing to India, the concept had changed quite drastically. Most of the big corporation still outsource their IT infrastructure as there is a technology stack which is required and cannot be found in house within their system.

While it has been fashionable to employ some coder to do some project in house , the majority of the outsourcing work by the Fortune 500 are still done by the Accenture, Cognizant and Infosys with their coders and consultants all over the world.

Actually, if you had bought the outsourcing industry you would have done really well! We were not so smart in 2008, and we are hoping to be smarter now.

We still believe the outsourcing work will continue. Most major corporation will need some form of outsource IT work to continue to bump up their remote working, increase the productivity of their worker. What if we can have a chance to buy a company similar to Cognizant and run by the best manager from Accenture? That sounds like a beast in the making.

The company we are talking about here is DXC Technology NYSE:DXC. Looking at the chart below, you know some caveat is coming.

This is in the special portfolio for a reason. We are expecting some changes in the business and we are experiencing it right now!

History:

DXC came about through a merger between CSC and Hewlett Packard Enterprise (HPE) company in 2017. In 2018, they spun out their U.S. Public Sector business known as Perspecta.

The de-rating of the company started in February 2019 when news of lawsuit by an ex-employee hit the news. The market seems to know something more as the share price continue to fall. DXC then delivered a disappointing quarterly report that sent its stock price through the floor with news of layoffs and office closures.

By September 2019, DXC announce that Mike Salvino will replace the long standing Chairman/CEO Mike Lawrie.

CEO:

Mike Salvino came with a pedigree like no other. Salvino had previously ran Accenture’s outsourcing business, is very highly regarded in the industry.

Throughout his career, Salvino has been a committed and articulate voice for skills development in outsourcing, and for the need to create career paths for outsourcing professionals. In addition to supporting the IAOP’s Certified Outsourcing Professional (COP) program, he has championed award-winning employee engagement and talent development programs in Accenture

-Outsourcing Hall of Fame

Right after coming onboard, Salvino informed investors of potential revenue runoff which means that clients are planning not to renew their contract with DXC.

Being totally transparent, Salvino had revealed that the revenue runoff had been due to DXC inability to deliver and not being proactive in building client relationship and not due to a migration to cloud (which had been the reason given by the previous CEO).

Going forward, management have to

keep the good stuff,

create a game plan to shake the culture within the firm and

dispose the non-core stuffs to lower debt and focus the company.

Keeping the good stuff:

While customers are planning to leave in droves, some stayed and some new one signed on for a reason. While most continue to believe that an outsourcing company like DXC exist as a manpower arbitrage play (selling in the US through lower manpower cost in Asia), this is no longer true.

DXC do have a technology stack and that stack do help them to gain contract within their certain industry.

Let’s get the positioning of DXC from the Sabre’s from the travel, transportation and hospitality sector.

Sean Menke, president and CEO of Sabre said, “Earlier this year, we announced that Sabre was embarking on a new transformational journey with Google… Throughout that migration, we knew it would also be vital for Sabre to partner with a third party to maintain the secure foundation of our existing systems while also modernizing our technology to meet customer demands. With the ‘new DXC’ playing this important role in our technology transformation, we fully expect Sabre will be able to better serve our customers, achieve meaningful cost savings and generate long-term growth opportunities.”

And Topsail Re from Insurance Sector

“One of the core aspects of our business strategy is simplifying the reinsurance process for all parties and providing our partners with a stable, long-term platform,” said David Johnson, chairman and chief executive officer, Topsail Re. “DXC’s solution was the most comprehensive application of its kind and will save time and reduce costs through automation, as well as provide the reporting tools we need to meet regulatory requirements.”

Do also take note that DXC is the leading provider of core insurance systems, serving more than 80% of insurers in the Fortune Global 500.

Creating a Game Plan:

The game plan for revitalising DXC are pretty straight forward,

Fixing troubled account - Almost done

Look at margins by simplifying the organization - In Progress

Cross sell - In Progress

Build the team - Almost Done

Let weigh how well DXC is doing.

1. Fixing troubled account:

The good news, since Covid-19, they have been receiving praises from their customers.

And then they received good news that some contracts are saved such as the contract with Sabre which is supposedly going to run off.

There are some misses as well such as Geoscience Australia moves to replace IT services deal with DXC…

Salvino claimed that he is getting on the call with his team every single week to stabilise the business and overall he seems to be doing a good job. In June 2020 earnings call, Salvino confirmed that DXC had fixed 35 out of the 40 challenged accounts.

Covid-19 Impact:

70% of DXC revenue comes from outsourcing and the 30% comes from project. The beauty is that not all the project is discretionary.

85% of their revenue comes from industry which has medium to low impact from Covid.

15% of their revenue comes from industry such as travel, hospitality, consumer and retail which is most impacted by Covid.

So Covid is going to matter but not cause so much headache to them till it will derail their transformation plan.

2. Simplifying the organization

They are currently delayering the management and also actively optimising cost to match the revenue.

If it is just about cutting cost, then this is no different from the previous DXC. They are actively hiring people as well! Check out their Linkedin profile.

They are looking at lots of hires as well and giving a pay raise for the employees who had made a difference to the customers.

3. Cross Sell:

They have 200 customers out of the Fortune 500 so there is plenty of chance to cross sell. With the intention to migrate to the cloud, they have plenty of chance to engage their customers continuously. That sounds good enough for us as cross-selling is always tough to track.

Build the Team:

Other than the CFO, the executive team, the Chairman and the Board of Directors had seen new faces.

Chairman:

Ian Read, former chairman and chief executive officer of Pfizer came on as Chairman of DXC in February 2020. Ian Read is the CEO who is credited with cutting costs, pleasing shareholders and fixing Pfizer’s R&D operation.

Chairman Read did a similar game plan when he was over at Pfizer. We believe that Read would be able to advise Salvino on how to navigate this minefield successfully.

Read cut head count from 130,000 to a low of 80,000 at the beginning of this year, raised $32 billion by selling off extraneous divisions and got seven drugs approved. He made Wall Street salivate over the idea of breaking Pfizer into two companies, a slower-growing business that sells older medicines and a hot one that focuses on breakthroughs. Though the paring down cut sales 27% to $50 billion, annual net income has increased 10% to $9 billion. The market has applauded: Pfizer shares are up 94% over Read's tenure

-Forbes

Disposing the non-core:

Salvino and the CFO - Paul is having a race to look for strategic alternatives for the segment below.

CFO is out in the marketplace working on strategic alternative while the CEO is leading the effort to redefine the business. From the look of it, the CFO is winning. DXC had announced numerous asset sales.

On March 10 2020, DXC announced the sale of U.S. State and Local Health and Human Services to Veritas Capital for US 5b. This sale is expected to close at the end of the year. The asset is sold at 3.5x sales (USD 1.4b).

On July 20 2020, DXC announced the sale of DXC’s Healthcare Provider Software Business to the Dedalus Group for USD 525 Million in Cash. This is expected to close by March 2021.

Two down and two more to go!

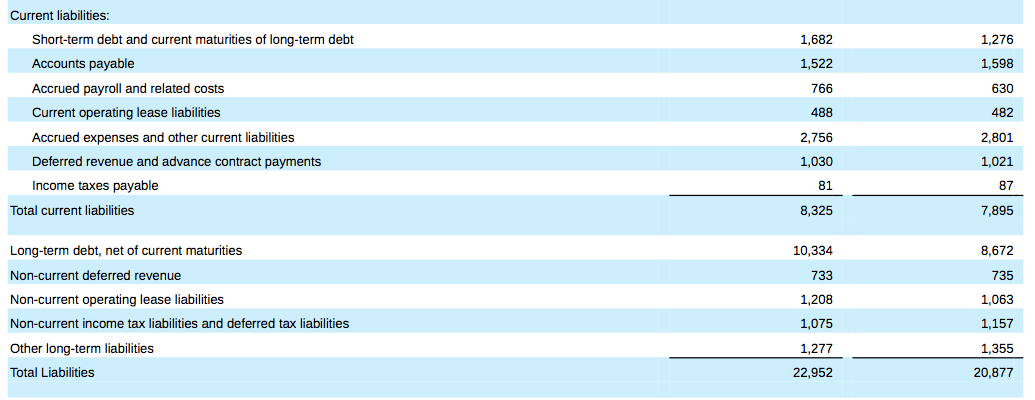

Balance Sheet:

DXC had basically raised USD 12b in debt, they had paid down their term loan, extended their maturity schedule and modified their covenants to give them ample runway to execute their transformation. They should have USD 600m worth of debt coming due in the next 2 years.

Coupled that the management had indicated that the after tax proceed from the sale will be used to pay down debt.

With cash of USD 5.5b and another USD 5.5b coming in from the sales, coupled with 2.5b from working capital, DXC has negligible debt obligation by year end.

Normalised Earning:

If the company returns to low double digit ROE or even approached what Accenture are doing, we will expect a ROE of 10 - 20% with normalised earnings of between USD 400 - 800m. That will bring about a re-rating of the shares way above current valuation.

The way we like to value the company is not in comparison with others but within itself. They had sold off their non-core assets and that had already garnered USD 5.5b of cash. We believe that current operation has a lot of value left.

With an equity value of USD 4.5b, and a market valuation of USD 4.8b, DXC is clearly undervalued based on possible normalised earning or on the balance sheet basis.

Average Purchase Price: USD 16.903

Holding Period: Till market recognise the turnaround

Disclosure: At the time of publishing Wee Hiang has a position in the above company. Holdings are subject to change at any time. This report, and disclosure, should not be considered to be a recommendation.

Update: CFO Paul left DXC to join as CEO of U.S. State and Local Health and Human Services. We like Paul as he is the only old timer left and he is able to keep up with Salvino. On the other hand we have been contacting some DXC staffs and they had confirmed that things are changing on the ground. People are feeling uncomfortable but we guess that is good for the long run. We accumulated more shares yesterday at USD 18.80 as the price retreated.