SembCorp Marine - Rights Issue and SembCorp Industries Demerger exercise

And how we are going to profit from it.

SembCorp Marine Ltd - SGX: S51 (SCM) announced a right offering and SembCorp Industries - SGX: U96 (SCI) had agreed to the rights offering and a plan demerger for SCM. This will allow the two companies to be separated and have renewed focus on their core businesses.

Whenever there is a demerger, we think that it is time for investor to pay more attention. Demerger usually involves the distribution of shares (in this case SCM shares) to SCI share holders. As SCM shares are sort of distributed for free to SCI shareholders, there is usually quite a bit of selling pressure on the distributed shares. Therein lies the opportunity to purchase demerger shares at a good discount.

At the time of writing, share price of SCI had risen by 33% which indicated that market is in favour of the move.

On the other side, SCM share price had fallen by 31%. As SCM will be issuing a 5 for 1 Right issue at SGD0.20, the share price had dropped.

SCI had undertaken to subscribe for up to SGD 1.5 billion of the Rights Shares by setting off the SGD 1.5 billion outstanding under its Subordinated Loan extended to SCM. This means that SCI will convert the Subordinated Loan into equity of SCM with Temasek agreeing to sub-underwrite the remaining $0.6 billion making the fund raising process to be SGD 2.1 billion. The proposed first step of the fund raising will result in possible shareholding as below.

Our expectation is that only minority of SCM public shareholders will choose to subscribe to the rights issue. This means that SCI could possibly end up with the higher range of the shareholding (60.9% - 69.6%) after the Rights issue has ended.

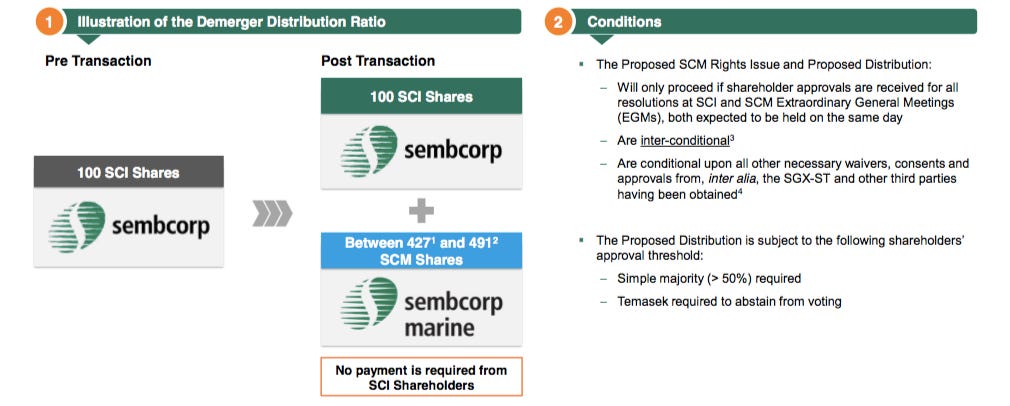

A demerger exercise will follow after that in which SCI shareholder may receive between 427 - 491 SCM shares for every 100 SCI shares.

By spinning off SCM, SCI would be free off the negative contribution by SCM. In addition, by getting rid of SCM, SCI's balance sheet will be clean as SCI no longer needs to consolidate SCM balance sheet. This will leave SCI focused on their Energy and Urban portfolio while SCM will focus on Offshore and Marine portfolio. If your inclination is to buy SCI and collect and sell the SCM shares, do understand that it would be the inclination of most of the investors.

Investors will usually prefer SCI than SCM as SCI holds a portfolio of stable assets such as energy plants and water works produces recurring revenue and returns. But do take note that energy plants are often subjected to government tariff and economic of that particular country. Do refer to our previous article if you are interested to know our thoughts on energy producer.

In gist, the operation of public utilities in a foreign country usually requires local knowledge. SCI expansion into foreign countries had exposed them to multiple foreign investment risk showing that they may not have the necessary local knowledge to execute on foreign soil.

In SCI's 20194Q profit guidance report, SCI took an impairment of SGD 158 million on UK Power Reserve (UKPR) - UKPR is a UK based flexible energy operator with a portfolio of small scale, fast ramping power generation assets and rapid response batteries that is connected at distribution points. This asset was purchased for EUR 216 million (SGD 338 million in current currency term) in 2018. In regards to the investment in UKPR, taking a 50% impairment within a year is just not acceptable. It basically meant that the management had overpaid for an asset. Directionally, we think that SCI will be getting very little value out of UKPR (thou the SCI's CEO McGregor thinks that directionally they had got it right!). If writing down an recently acquired asset is a right direction, then we guess that there is really no wrong direction after all!

In addition, SCI also registered a SGD 64 million impairment of their water business in Chile, a SGD 23 million impairment of their water treatment plant in China. In total, SCI recorded an impairment of SGD245 million in 2019!

While the demerger will free SCI of SCM, SCM would also be getting a relative reprieve on their balance sheet. The subordinated loan will be converted into equity with another 600 million in cash to bolster their balance sheet. As oil prices continue to normalise and demand slowly creeping back, SCM may just be able to survive till the dawn rises again. SCM will have a cash of almost SGD 1 billion against bank borrowing of SGD 2.8b. While debt level still remains high, the runway for SCM had gotten longer as they continue to renegotiate their loans.

Using a thought exercise, so how do we play the demerger theme? Our guess is that the rights issue would be undersubscribed. This also means that there would be a chance to apply for excess rights allowing an investor to get additional shares at SGD0.20. Post demerger, we would expect additional selling pressure from investors who do not want to hold on to SCM shares, thus depressing SCM shares further. On an overall basis, we would not expect SCM share price to fall below SGD 0.20 which is a fraction of SCM net asset value and seems to be price in favour on the right share doing well.

So what will we be doing? We will wait for the rights offering to be finalise. When it is, we would expect another round of selling of SCM as shareholders suddenly realised that they need to fork out more cash for this dud.

We will buy a the minimum number of shares (for e.g. 100 shares) in the market while subscribing to excess rights (19:1) at SGD 0.20. In the event that the rights are undersubscribed, we would have excess 19 shares at SGD 0.20 and 1 share at SGD 0.45 (current market price). This will bring our average price to be around SGD 0.22 which is an excellent entry price for a company currently being supported by Temasek and de-risk through SCI 1b stock conversion.

We had outline our trade and we will see how we can make some quick buck on a demerger/rights offering exercise like this.