Demerger of Yangzijiang Shipbuilding Holdings (YZJ)

Which will face the drop? The ship or the financial?

I am always on the look out for de-merging exercise.

If you are keen on both assets, then it is always good to buy prior to the de-merging exercise.

If you are clueless (like me), then it is best to wait for the de-merging exercise to complete.

Sometimes, if there are huge selling pressure, it will allow some speculators like me to pick up some shares on the cheap.

Looking at the steep rise in price since 15th March, I have a feeling that most people would like to own both YZJ and the soon independently listed financial arm Yangzijiang Financial Holding (YZJFH).

YZJ is valued around SGD 6,125mm (21st April 2022) prior to the de-merged asset.

Since it is currently trading ex-entitlement for YZJFH, the market seems to be assigning a value of SGD 2,625mm (6125 - 3500 = 2625) for YZJFH.

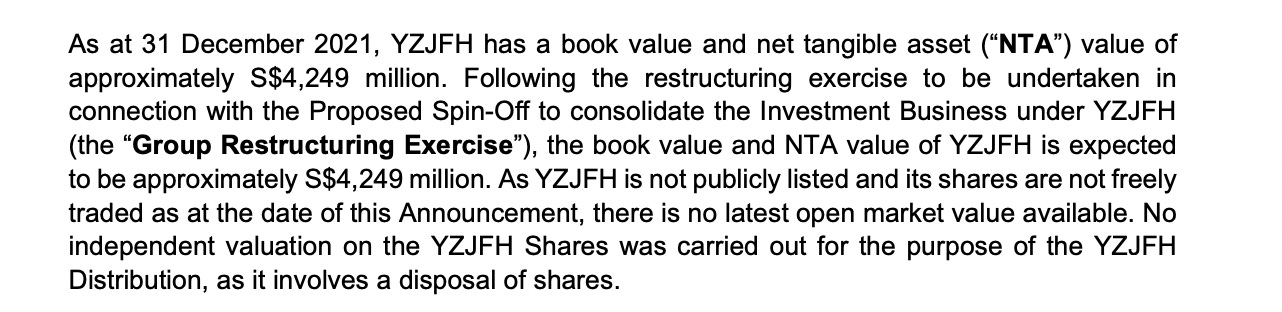

From the announcement from YZJ on 1st April 2022, it seems that the NTA of YZJFH is around SGD 4,249mm.

Thus the market is assuming that YZJFH will be trading at around 61.77% of its NTA.

I am unsure how all these would trade but if YZJFH is sold down to < 50% of its NTA, I think that would start to look interesting.

Since YZJFH will have around 3,951mm shares.

The perceived market price of each share should be around SGD 0.66 - SGD 1.075.

I am looking to pick up YZJFH at < SGD 0.50?

Why would it trade to that level?

Investors has been asking for a split for a long time.

While the reason usually given was that YZJ would trade at a better valuation ex-YZJFH, it also implies that investors are just not so keen on the financial side of the business.

With a general weakness in the market and international investor avoiding everything Chinese, there could just be a good chance that the YZJFH will be sold down by most institutional investors.

In the meantime, I just wait for the price to come to me.

if it comes…