Cyclical Portfolio #1 - Uranium Participation Corp

The cleanest power in the world

Our thesis for cyclical play is always the same. There must be significant supply destruction and significant period of low prices. While we do not know when the prices will increase, we are sure that if prices improve the wait is worthwhile.

Uranium interesting as the supply of Uranium had been dropping for many years. Economics 101 says that when supply decreases, prices will go up. The reality is that supply can decrease but prices can stay low for long period of time due to inventory stock up of the past.

The high prices of Uranium in 2007 brought about a 10 fold increase in production in Kazakhstan. Fukushima happened and prices are brought back to earth for the next 10+ years.

We like Uranium as it is a commodity that still can be analysed. It helps in someway that the market is opaque as well.

There is a couple of major producers of Uranium and the customers are just price takers or to be exact - takes any price (spot or long term contract).

We do not want to invest in the miners as we do not know when the uranium market will recover, but we do not mind if it is a cheap call option on the mineral.

We believe that the cleanest and cheapest way to invest in Uranium is to invest in Uranium Participation Corp (UPC) - TSE: U.

The downside will be a widening of the discount to NAV while the upside will include a change in perception towards nuclear or a supply shock that is unanticipated.

Destruction of Supply:

During the last major up cycle in 2006-2007, uranium averaged over $100 and peaked at $137. Subsequently, global production increased by nearly 40%, driven mostly by Kazakhstan.

The market had spent a number of years to run down excess inventories. As a result of prolonged low uranium prices, supplies had been reduced.

In January 2018, Cameco Corp. (Cameco), the largest Canadian uranium producer, suspended production at its McArthur River mine, the world’s largest high-grade mine and Cameco also briefly suspended production at the Cigar Lake mine in March 2020 till September.

Kazatomprom JSC (Kazatomprom) has confirmed that it will maintain its already announced 20% reduction in uranium in 2021, but in addition will also ‘flex’ down production by 20% in 2022. Kazatomprom accounted for 25% of global uranium production in 2019 on its own, with Kazakhstan accounting for 43% in total.

Except for Covid-19, there are no more any disruption to the supply, making the environment feeling benign and safe for now.

Price Agnostic Buyer:

Demand for uranium is inelastic as

the cost of Uranium is a minor part (4%-5%) of the total cost of generating electricity

supply is usually negotiated through long term contracts

uranium buyers do not go out and buy more when it gets cheap.

Thus, even when uranium prices continues to tread lower, there is no increase in demand making uranium spot prices a bad indication for the real demand and supply situation. The better way to track uranium demand is to use the long term prices.

The spot prices and the long term price differ sufficiently for the reason stated above.

Due to the closure of their mines, Cameco and Kazatomprom are both going to the market to buy at spot prices rather than taking it from their inventory.

Structure of UPC:

UPC invests in holdings of physical uranium without actively speculating or trading on changes in uranium prices. UPC owns physical uranium and trades at a discount to spot and long term market price.

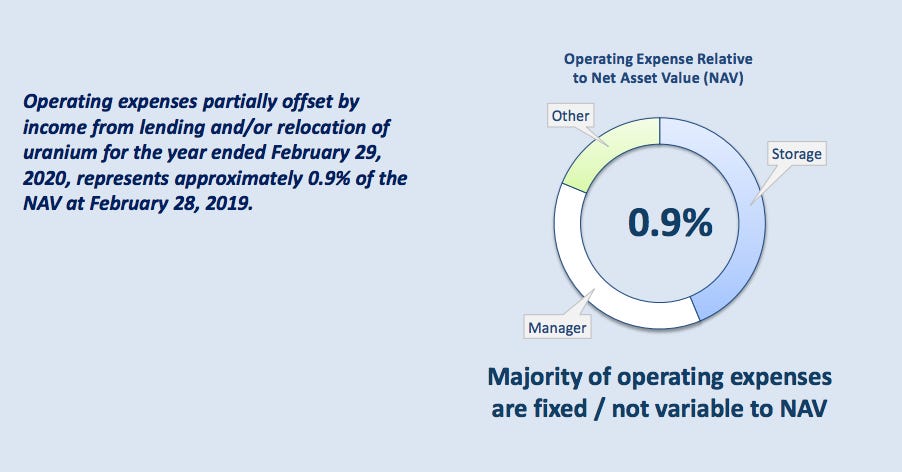

At the same time, UPC has a carrying cost of less than 1% a year, we believe that it is a great way to buy an uranium option on the market.

In the extreme case of a major upswing in prices, the upside for UPC will most likely be 2-3 x, instead of 10 - 100x for a junior miner but an investment in UPC carry minimal downside risk with a decent upside potential.

Financial engineering:

When UPC is selling at a discount to NAV, they will sell Uranium and repurchase shares.

On the inverse, when the share price is selling at a premium to NAV, they will sell shares to purchase uranium.

This means that on a theoretical basis due to UPC arbitraging behaviour, UPC should trade at par.

The reason that a discount continue to exist suggest that

the volume of the shares for sale is too huge for UPC to absorb on a share buyback basis

there is an inability to sell uranium at spot prices as spot demand is limited or the spot price is unattractive

investors sentiment continue to be affected by headline news regarding the supply and demand of uranium

The 2-3 x return bet on UPC depends on the

continued destruction of supply from major producers

change in media/investor perception on the availability of uranium

change in media perception on nuclear power

But to get an return on UPC, we just need the NAV discount to shrink and it is bound to happen at some point unless uranium prices collapse in a drastic manner which we see little chance of happening.

So overall, we think that

long term prices of uranium will continue to tread up

the discount to NAV should contract

any unexpected supply constraint may pop the uranium prices

Average Purchase Price: CAD 4.34

Holding till: When lady luck shine on us…

As usual, do poke a hole at our thesis above and we will try to defend it till we can’t.