Company Update: REX International

20220325

I had released my report on REX International (REX) on the 24th June 2021 when crude prices are treading along USD50.

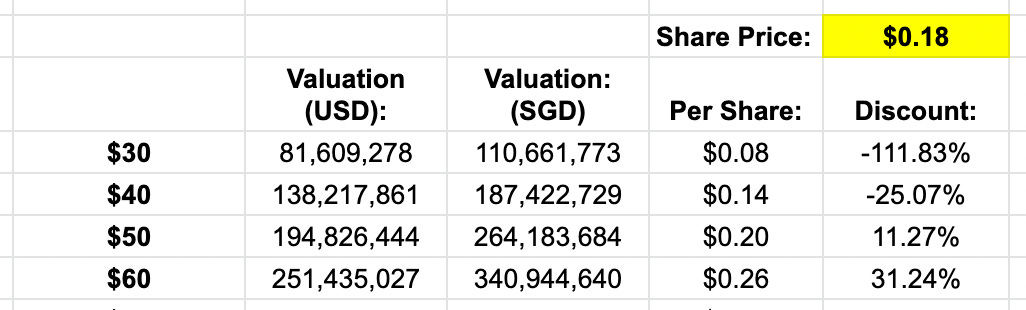

The only reason why REX is interesting to me is that it is small and simple enough to do a discounted cashflow (DCF) analysis.

I bought it at the entry price of SGD 0.18 and the valuation per share is SGD 0.20.

The purchase is really just a pure bet on crude price rising with a slight margin of safety (11.27%).

The interesting thing is that REX basically track the price of crude from USD 50 to slightly less than USD 100 before the relationship starts breaking down on 28th Feb 2022 just before crude prices hits >USD100.

Since crude prices are at > USD100 now, we should be valuing REX at > SGD 0.50? The discount has widen > 30% as crude prices goes up.

Some potential hypothesis that can be draw out from the observation:

Lots of people are selling REX when crude prices hits USD100?

Crude price at USD100 present a clear psychological barrier to buy?

Crude prices are due for a fall to USD80?

Singapore market is relatively inefficient?

At USD100, expenses will increase and net margin of REX will shrink?

Changes in shareholder expectation in the capital allocation policy?

Maybe all DCF calculation is a farce?

I do not know how to value an exploration and production company…

If you believe that crude prices are going to stay elevated above USD100, then this could be a wonderful time to purchase REX as the discount has never been wider.

As for me, I am happy to hold on to my current position in REX as a hedge for my overall portfolio.