Capita PLC

When you become the blue eye boy again...

CAPITA PLC, LON:CPI - GBX 20.48

2023 September: Capita PLC purchased at an average price of GBX 17.1 provides consulting, digital, and software products and services to clients in the private and public sectors in the United Kingdom and internationally. It operates through Public Service, Experience, and Portfolio divisions (for sale now).

It used to provide the regular outsourcing services like solutions for finance and accounting, procurement, property and infrastructure, travel and event, and workplace administration, customer experience transformation, contact management, collection and complaint handling. In recent times, it is executing the above through system and software, data and analytics.

Capita is a classic case of an over aggressive acquisition and indigestion from past years. They started to lose money on every contract win and needed to slim down in order to survive. Jon Lewis was brought into Capita to save the company and as just the turnaround seems to be happening, a hacking incident in March 2023 brought the company back on its knees again.

Since the hacking incident, Capita had continued to announce a slew of contract wins. Divisions continued to be sold off and insiders (CEO, CFO and the CEO of the Experience Division) have bought stocks using their own money.

The second half should be a kitchen sinking quarter with losses from the hacking incidents and restructuring all thrown in. FY 2024 should look a lot better. This company should be valued based on its moat in winning public contracts. With better digital capabilities, they should be poised to improve operating margin by cutting manpower and improving their margin profile.

Book to bill ratio for the public service division should continue to remain above 1x. Full year adjusted profit before tax should be around £60m valuing the company at 6-7x PE. That is not an attractive valuation but if the margin could be doubled, then at current price Capita could really look like a steal.

With the kitchen sinking exercise happening in 4Q FY2023, the bet would be that the FY2024 revenue and operating margin would be much higher than FY2023.

Capita will be a sell if the new CEO deviates from the pre-arranged plans or if the turnaround engine starts to sputter and operating margin for FY2024 missed by a big margin.

Written on: 21st November 2023

I bought Capita PLC (Capita) in March 2022 for 21.9 GBX and then swiftly sold it in August 2022 for a 17% return. In hindsight, that was a bad decision.

In my previous post, I said that the holding period is for one year.

If I had followed my own advice, Capita would have hit a high of 42.64 GBX on March 2023 before succumbing to gravity of bad luck or poor execution.

Capita has since derated significantly from that high of 42.64 GBX to 18.88 GBX

The crash in stock prices came in March 2023 when Capita was subjected to a hacking incident.

This hacking incident has totally overpowered the story of the turnaround.

Then on 31st July 2023, it is reported that the turnaround specialist CEO Jon Lewis is stepping down (seemingly from the hacking incident).

While everyone is focused on the hacking incidents and its effect on this year's current earnings, my focus continued to be on the turnaround that should be happening in FY2024?

The turnaround looks like it is already happening if you can look past FY2023.

There are usually a few phases in a turnaround.

Selling of non-core assets

Directing resources to their core businesses

Streamlining of their core businesses

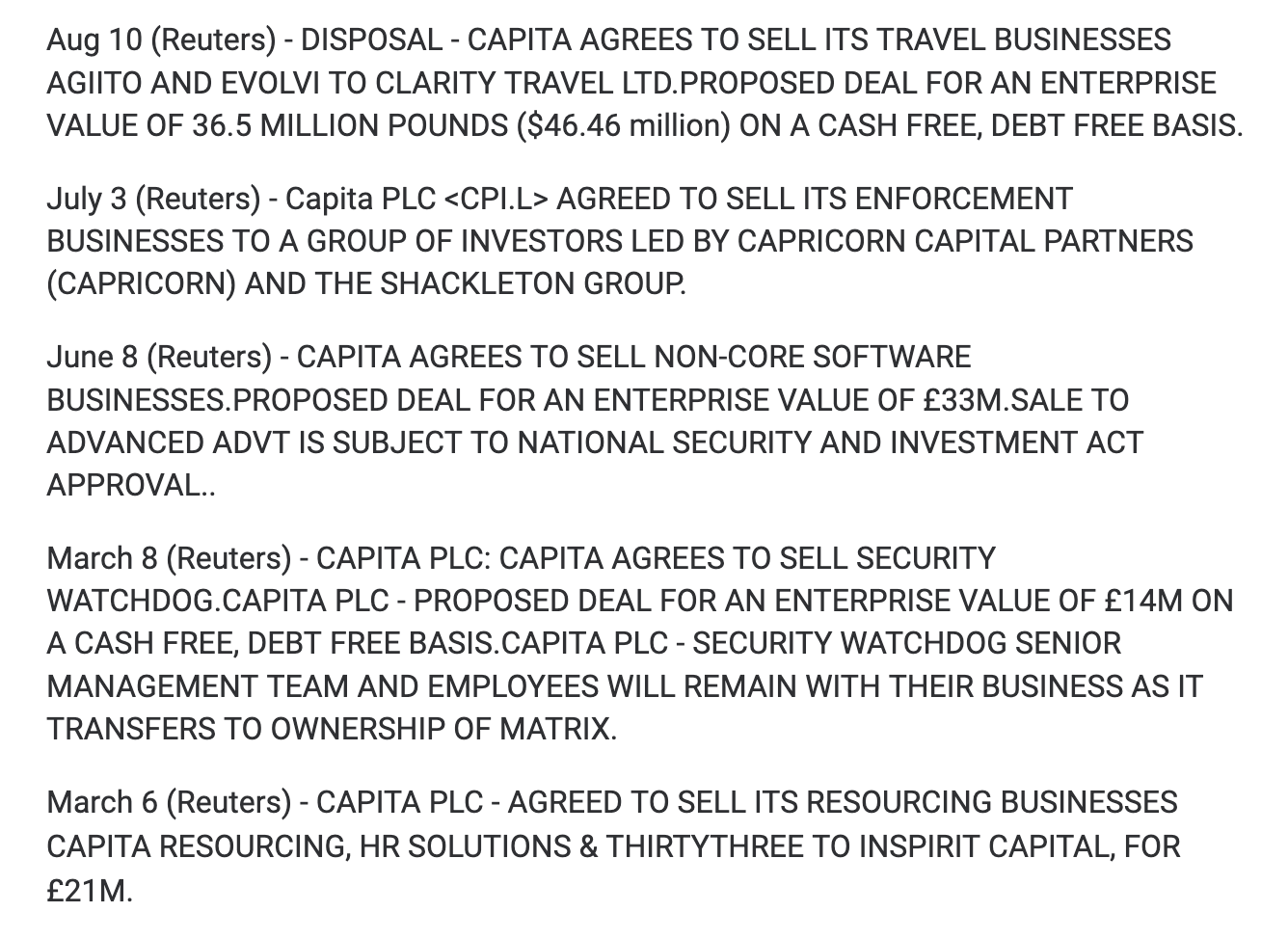

1. Selling of non-core assets

The wording (penultimate) surely indicate that they are at the tail end of their asset disposal.

2. Directing resources to their core business

These are the public contracts won after their hacking event and it seems that the government agencies continue to put trust in Capita.

As of 21st Nov 2023, Capita continues to affirm their guidance that the company continues to trade in line with its expectations with a total contract value (TCV) of £2.85bn year to date compared to 2022 full year TCV: £2.59bn.

3. Streamlining of their core business

It seems that the old CEO (Jon Lewis) is going to do the new incoming CEO (Adolfo Hernandez) a favour by kitchen sinking most things by FY2023.

Growth can come from either an increase in revenue or a decrease in expenses which should boost operating profit. It seems that Capita is going to get both going at the same time.

Risk:

Turnaround is a risky business. Most ships sank to the bottom of the ocean. The operating margin could continue to worsen despite their cost reduction programme.

Despite the management’s best effort in selling down businesses (which I never knew existed within Capita) and paying off debt, debt level remains high.

Bet:

The main bet remains that the recent contract wins signify that with Capita being the flag bearer for UK government outsourcing contracts, the contracts win should continue?

If Jon Lewis who is leaving the company could cough out some dollars to bet on a turnaround, there is a good chance that the turnaround is happening soon?

I think the blue eye boy’s eyes should be getting bluer again.

Do your own research and I may buy and sell the above-mentioned stocks at any time.