2024 Week 25

China Merchant China Direct Investment, Natural Food, Gross Margin

China Merchant China Direct Investment 133.HK - when the sparks fail to fly, will the stock fly?

I spoke on Week 20 about CMCDI.

While everyone's idea of a good entertainment is a good Korean drama with some spark with a pretty boy and a stunning lady, my idea of entertainment is to see the “sparks” fly between bad boy Brian from Argyle Street Management (ASM) and stunningly conflicted Elizabeth Kan - one of the board of director from CMCDI during their AGM.

Instead of sparks, we got a respectful ASM at the AGM.

The reason is the bad boy did not speak at the AGM and left the mic to his colleague, the mandarin speaking politically correct Star Gui. He is definitely a “star in the making” for his respectful speech to the BOD.

So is this the typical activism in Asia? Really aggressive online presence coupled with a really muted offline performance? Or is this the norm for all activism campaigns around the world?

Anyway, back to the meeting.

It looks like ASM has almost 44m votes wrap up on their side.

Quoting from ASM unlockvaluechinamerchants.com,

Given that China Merchants Group and Victor Chu (and their respective affiliates) own 29.6% in CMCDI, that means: almost everybody else (including sophisticated institutional investors) wants Elizabeth out.

Now they need more shareholders to move over to the dark side and vote.

The problem is that I still do not know which side Lazard (one of the major shareholder of the firm) is standing with.

If I am Lazard, it is time to shop around. They may choose to go with anyone who provides them the “best possible deal:. Since ASM is unwilling to be see acting in concert with any other shareholders, it meant that Lazard could be talking to CMCDI?

The varied possibilities of Lazard working with CMCDI could throw a spanner into ASM’s plan?

My key takeaway for the AGM,

Interim dividend is coming?

Meant divestment is coming?

BOD seems to be comfortable to consider value enhancing measure

Some share buyback?

If ASM get lucky, they may have just enough votes to remove the manager in November

So a reduction of manager fees will be coming?

So the melodrama will drag on to November and the episode 2 will resume. This time the main character will not be Elizabeth but her boss Victor Chu.

I am not going to speculate on what value enhancing measure CMCDI will do but either way I think continue to favour the thoughts of getting a decent return from CMCDI at current prices of HKD 13.56 before the year end.

Natural Food - Everything is natural or so they say…

Natural Food International Holding Limited, an investment holding company, engages in the processing and sale of natural health food products in China. The company also offers management and administration services. It markets its products through a network of concessionary counters; channel networks; and online channels, including e-commerce platforms. The company was formerly known as Roomy Development Holdings Limited and changed its name to Natural Food International Holding Limited in May 2018. The company was founded in 2007 and is headquartered in Shenzhen, China.

-Tikr.com

I understood a little more history on their listing during my second meeting with them and I think I can make some sense of their business or capital allocation decision.

Natural Food listed when their offline business is declining.

Just before Covid hit, their pivot into online sales managed to catch the wave of online purchases.

Leveraging their brand recognition, their new online products gained traction and managed to offset their declining offline sales.

Their success and possibly the growth of online sales of food products attracted tons of competitors into the online space.

After the end of lockdown, renowned competitors like Beijing Tonrentang also noticed this trend of health food online and have started selling similar products offline

Online food products operator also started to move offline albeit with huge losses

May it be in the online or offline space, the question is how is Natural Food going to handle all these old and new competitors? Natural Food may have a branding advantage for now but can they continue to maintain a premium pricing in a weakening market where product is inherently hard to be differentiated in an online world?

The uncertainty on the success of their new products meant that the management knows that the company is on a knife edge. They need the excess cash to be lying around just in case anything trips up. There is much uncertainty when there are so much competition.

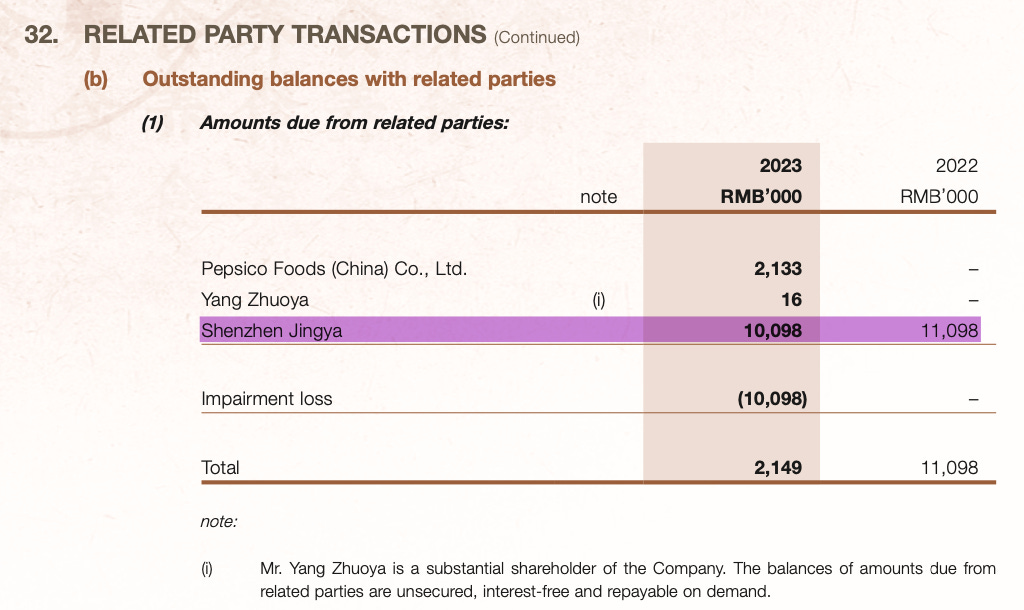

In addition, in the latest annual report, there is an Impairment of RMB 10M of financial assets due from related parties - Shenzhen Jingya. This is a potential red flag which could warrants more explanation…

Thinking about gross margin:

My simple thinking in the past has been that the higher the gross margin, the better the business.

There is nothing wrong with that thought but the better question to ask would be

What are the factors that help the company maintain or even improve that gross margin?

That sounds better?

An even better one?

What are the things that the company is doing that may decrease your gross margin but help create a long lasting moat for the business?

The question is not about a higher gross margin but what is the gross margin that is left untapped. If you have tons of gross margin left untapped, it means that it is hard for competitors to come in. If you have tapped out all the last drop of gross margin, expect some serious competition for your business.