2024 Week 21

Nam Cheong, Water Oasis, Perfect Medical, Semler Scientific

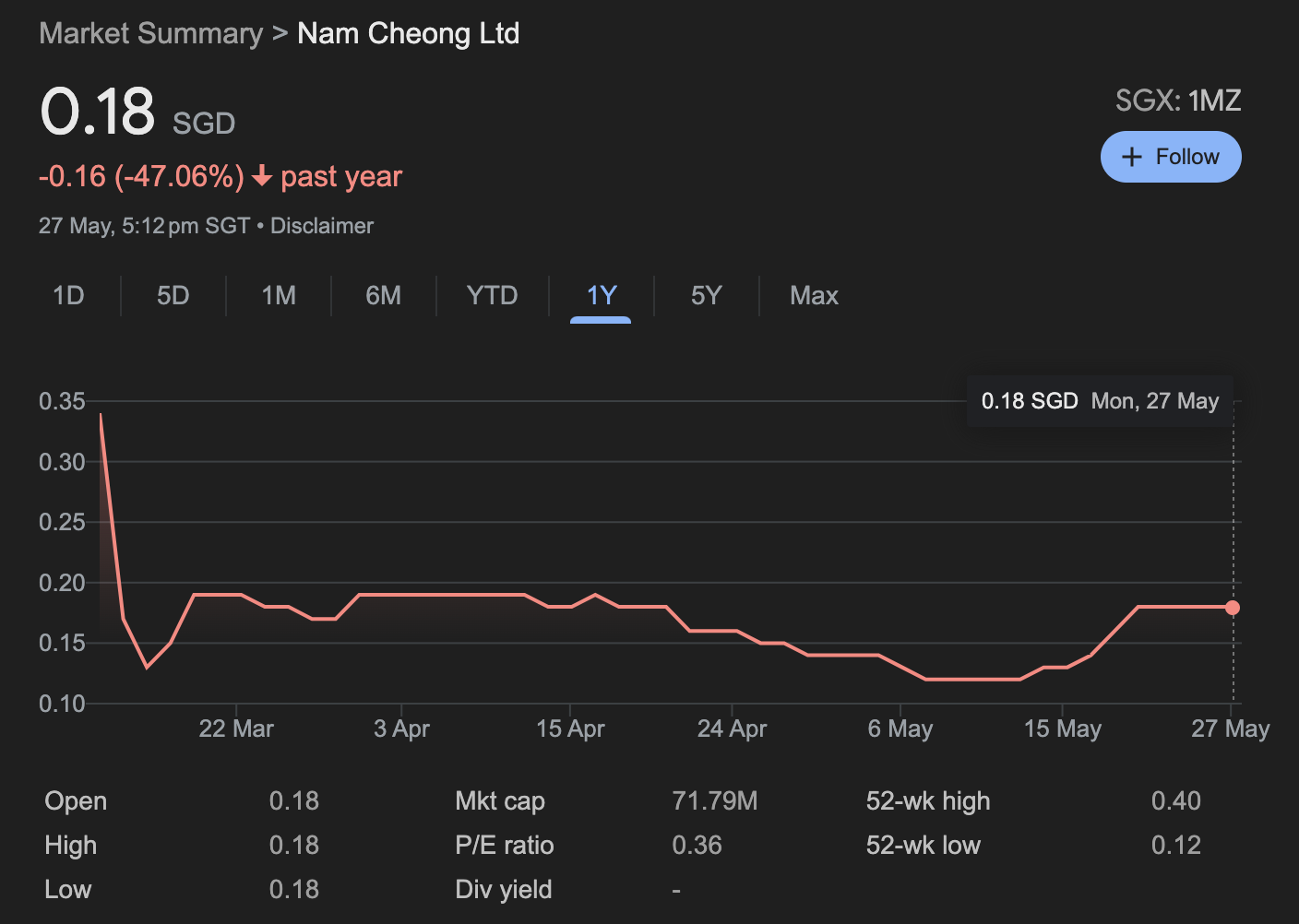

Nam Cheong - the phoenix or the cat with nine lives?

After having some good experience with Mermaid Maritime, I continue to dig for treasures in the marine and offshore sector. What used to be a thriving segment of the SGX prior to the oil exploration bust, is now the land of the restructured companies.

Nam Cheong provides shipbuilding and vessel chartering. The company builds and charters various vessels, including anchor handling tug supply (AHTS) vessels, platform supply vessels (PSVs), multi-purpose support vessels, maintenance work vessels (MWV), accommodation work barges (AWB), safety standby vessels (SSVs), and landing crafts.

The main attraction of Nam Cheong is that it is just coming out after restructuring their debt.

Things are messy and there are tons of information gaps.

At any one point I have many more questions than answers.

How many shares are there on issues now and are there going to be more shares being issued?

What are the effective interest rates they are paying for that debt?

What is the schedule for paying down that debt and the covenant imposed on it?

What are their ongoing capex and depreciation?

How much cash flow is being generated to reduce its debt load?

What are the charter rates for each type of vessel and on which part of the cycle it is on?

Are there more vessels to be delivered and how are they being financed or going to be used?

What are the values of their JVs and Associates?

Who are their main customers? Petronas and???

Since re-listing Nam Cheong has been sold down.

The main culprit here is RHB, who being one of the main creditors prior to the debt restructuring, is choke full of shares and is keen to reduce their stake in Nam Cheong.

With still more questions than answers, I am going to be stay on the sideline for now.

Water Oasis and Perfect Medical - too much of a good thing:

A profit warning from Water Oasis -

is good enough to send both Water Oasis and Perfect medical tumbling…

The beauty of the beauty industry is that they have a customer deposit - “float” to build their business with.

The companies sell packages upfront to customers and then slowly fulfill that commitment over time. Between the customers paying and the final delivery of the package (it may be 6 sessions over 6 months), the beauty salon gets to hold on to that customer cash and do something with it.

The ugliness of anything or specifically this beauty industry is when you take a good thing and then take that to an extreme.

The way to ensure maximum recurring float-revenue is to sell as many packages as fast as possible. Since beauty therapists and sales staff remuneration are usually tied with sale of packages, the beauty industry created a selling organization which has perfected the art of selling to women - i.e pressure selling. The overselling of packages also meant that facilities are constantly overbooked and customers are unable to book an appointment slot for beauty therapy which leads to disgruntled customers and bad reviews.

Customer float is like a drug that is hard to wean off. The moment you structure the organization around a singular flawed metric to maximize return, the organization just turns into a self perpetuating machine of bad customer experience.

When everyone in the industry is using the same strategy, it is often time for a beauty upstart to turn the industry on its head. I foresee that going forward, the most successful beauty company would be the company which eschews the idea of selling packages - going back to basics to provide the best customer experience in a cost effective way.

Semler Scientific - my cardiovascular obsession:

I had spent the past few years obsessing over every aspect of my health and that has somewhat led me down the path of reading up on pharmaceutical and medical technology companies.

Semler is a smallish medical technology company focused on helping healthcare providers diagnose and treat chronic diseases.

Semler received FDA approval for its product - QuantaFlo in 2015. QuantaFlo, is used to diagnose peripheral arterial disease (PAD) which is a circulatory condition in which narrowed arteries reduce blood flow to limbs.

There are some changes in the way their customers are being compensated for the usage of QuantaFlo and that is leading to some decrease in revenue

In March 2023, the Centers for Medicare and Medicaid Services, or CMS, announced the 3-year phase-in of the removal of the HCC code relating to PAD without complications from the Medicare Advantage risk adjustment model. 2024 marks the first year of the 3-year phase-in of the decreased economics to our managed care customers.

-Semler Scientific, Inc., Q1 2024 Earnings Call, May 07, 2024

So why am I flagging this here?

Semler is currently awaiting clearance from FDA to broaden QuantaFlo’s utility on a wider array of cardiovascular disease. This additional test will just require a software update to their existing devices (just imagine how Tesla send software upgrade to your Tesla).

Semler seems to be at the forefront of initiating preventative management programs in chronic cardiovascular disease. That means that QuantaFlo has the ability to save lives and reduce health care expenses.

There is potential competition from Medtronic with a product known as FlowMet. But with this reduced economics, I guess Medtronics will be the first to throw in the towel.

It always feels good knowing that I am backing an entrepreneurial company at a much reduced price, while knowing that someone bigger could just swoop in and take it out of my hands at a much higher price.