2022 Statistical #3: Berjaya Corp

When a CEO resigns and the value is in play

Take note that the note below are all speculation.

I am not an insider in the Malaysian stock market and all the information are glean from official press release and the Malaysian news.

I hold a position in Berjaya Corp and is in the midst of increasing the stake.

This following company is place in the Statistical Strategy.

Arbitrage:

Continued divestment of non-core units which will continue to lower debt.

Weighting:

Betting - Equal Weighting

Possible Catalyst:

Divestment of shares in Berjaya Food (Starbucks) and Seven Eleven Malaysia

Downside:

Management continue to suck on their thumb and continue business as usual

Holding Period:

1 year for more divestment and the improvement in result.

The news started on March 18th - Friday that Jalil Rasheed will be stepping down from his post to pursue his personal interests.

Since there is no announcement on Bursa, this could be rumour. But in Malaysia, most rumours usually “become truth” once it is reported by the Edge. Edge’s journalists seem to have the ability to get all the juiciest news before they are reported.

Then on the 21st March 2022 - Sunday, the Edge reported that a firm from Taiwan had written in as they are interested in Starbucks Malaysia and 7-Eleven Malaysia. In the article, Edge speculated that the Taiwanese party could be Uni-President Enterprises Corp.

Then on today (22nd March 2022), Berjaya Corp announced that Jalil Rasheed will indeed be stepping down and would be replaced by Ms. Vivienne Cheng Chi Fan and Mr. Syed Ali Shahul Hameed.

My speculation is that Jalil is leaving because there is a good chance that founder Vincent Tan is really considering the divestment of Berjaya Food and 7-Eleven Malaysia.

If Berjaya Food is taken out of the picture, then Berjaya Land would constitute the majority of Berjaya Corp revenue. Since Berjaya Land also owns Berjaya Toto, the promotion of Syed Ali to the role of Co-CEO Berjaya Corp seems reasonable and logical.

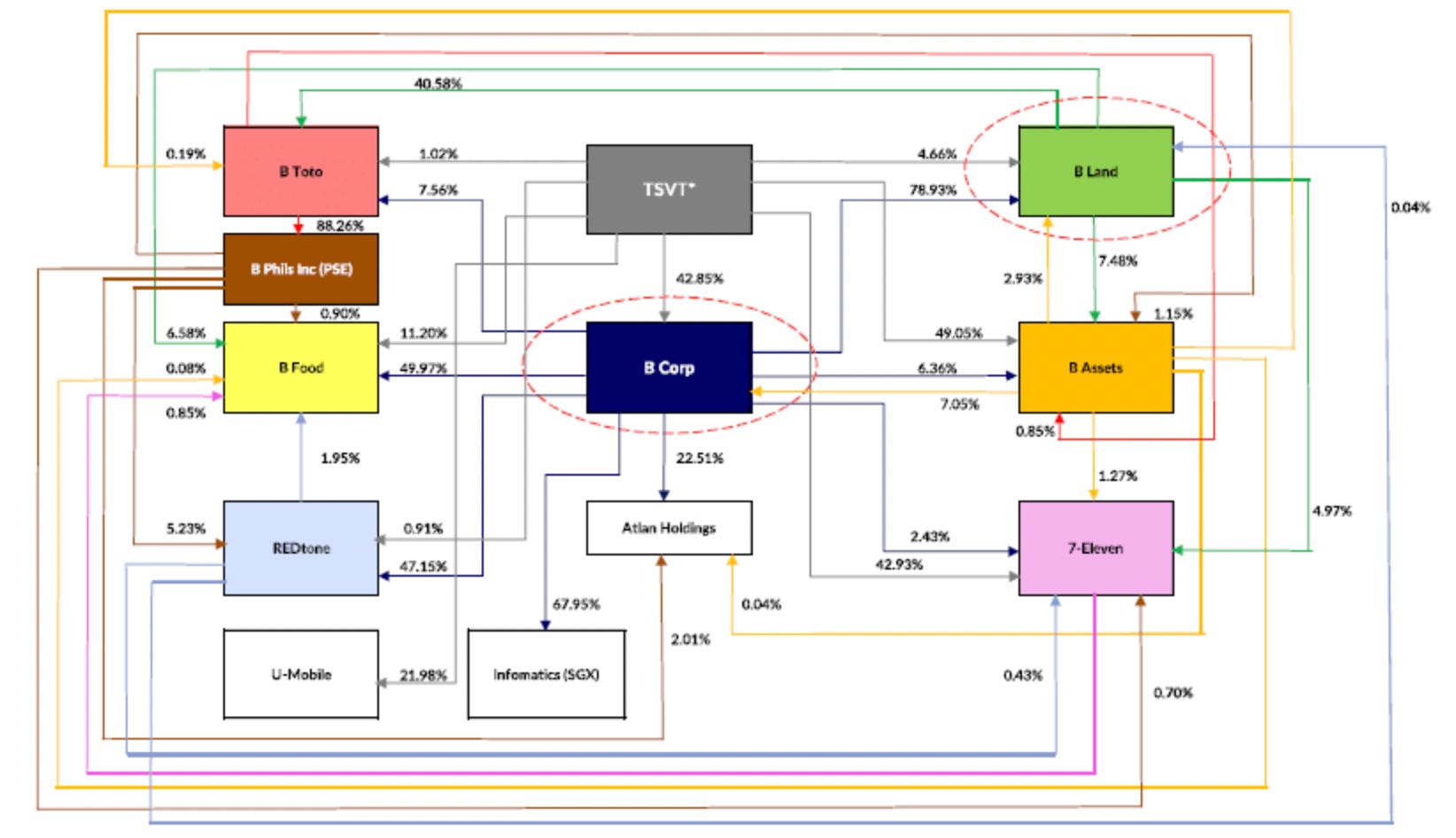

The current shareholding structure for the Berjaya group of companies currently looks like the below.

We could effectively ignore all the boxes and arrows above as the thing to understand is that most of Berjaya Corp valuation comes from Berjaya Land and Berjaya Food.

***speculation from here***

Once Berjaya Food and 7-Eleven Malaysia are sold, the cash received and the debt de-consolidated from Berjaya Corp should provide the share price a good bump.

The increase share price would allow Berjaya Corp to offer Berjaya Land’s shareholder a share swap (changing Berjaya Land shares for Berjaya Corp shares) allowing them to combine the two entities thus simplifying the complicated cross holdings.

Berjaya Land will cease to exist and Berjaya Corp would become the main listed entity.

The appointment of Ms. Vivienne Cheng as the Co-CEO is due to her capability in the area of finance to structure and plan for the above.

Upside and Downside:

The upside is that the sale of Berjaya Food really goes as plan and the cleaning up of the corporate structure will reveal a smaller, much profitable and more investable Berjaya Corp.

Berjaya Corp currently owns 49.97% of Berjaya Food and 78.93% of Berjaya Land which already account for more than Berjaya Corp current market capitalisation - MYR 1,220mm.

The downside is pretty much protected by the other assets held within the Berjaya Corp and the value of their other smaller listed entities.

Even if the sale of Berjaya Food did not come through, the appointment of Mr Syed Ali and Ms. Vivienne Cheng indicates that divestment should continue.

Overall, I like the setup that in the event that the divestment of Berjaya Food should happen, there is chance for a large upward re-valuation, while the downside risk is pretty cap due to the value of the various listed assets within Berjaya Corp as the divestment of the non-core subsidiaries continues.