2021 Quicktake #9: B2B2C in the Fintech space

One of the few profitable FinTech companies in the world.

With the Singapore FinTech festival coming around in November, I thought there should be some follow up on some FinTech companies around the world.

Since our last article on Maker Dao, the world had continue to invent new and interesting and FinTech business models.

Some look more interesting than others.

For investors who are interested in the exchanges, Coinbase looks like a buy even if most Crypto is not here to stay. I am a customer of Coinbase and the experience has been good.

NFT transaction marketplace like OpenSea looks like a business model that will continue to dominate if NFT use cases continue to expand.

While most of the above are really interesting, these are really use cases which has yet to “benefit” mankind. They are mostly unique use cases for the very privilege few or the trading mania of many in their spare time.

Other than Kaspi.kz which is really more of a traditional bank moving solely into the digital space, this Fintech company is doing something differently from the rest.

While I am enamoured with the business model, it has yet to shown that the business model can scale.

I am betting that it could.

It is also trading at a lower end and it could just be a worthwhile bet.

And it came from a SPAC and it could be one of those companies which is suffering from a lack of love right now!

This following company is place in the Super Strategy.

Arbitrage: Time/Growth

Weighting: Betting/Statistical

Possible Catalyst:

Announcement of new contracts

Downside:

Warrant dilution at USD 11.50

Holding Period:

< 2 years for new contracts to happen

While every other technology company is trying to get a bank license/charter, some companies are moving in the opposite direction. They are splitting up from their banking parents.

Not the As but the B nC:

BM Technology (BMT) was originally a unit of Customers Bancorp before splitting up and listed through a SPAC.

BMT serves as a go-between, linking financial institutions, consumers, employers, customers of nonbank companies and more with banking tech and compliance expertise.

The other company of comparison would be nCino which act as a layer of cloud-based bank technology company which was originally a unit of Live Oak Bancshares.

These two companies are interesting as

they are both truly cloud base companies which meant that they can and are able to onboard clients differently from the traditional players

they had build their stack up from scratch allowing them to reimagine how they could service their customers

they are spinoff from banks which makes their software/operation a tad more credible than the rest

they can serve a wide variety of customers, financial or not

While both looks interesting on a business model basis, BMT has a higher chance of being misunderstood by the market as

it comes through a SPAC listing which is an unloved segment

there are existing warrants which could dilute equity

and the business model is a tad more unproven

The news of Google winding down its Google Plex program dealt a blow to BMT’s share price. The Google Plex program is the highly anticipated program where a checking account will be linked to Google Pay.

BMT who is a partner would have benefited from its launch.

As the share price had treaded lower, management has been active guiding for decent result for the current year.

Overview:

BM Technologies, Inc provides state-of-the-art high-tech digital banking and disbursement services to consumers and students nationwide through a full service fintech banking platform, accessible to customers anywhere and anytime through digital channels.

BMT facilitates deposits and banking services between a customer and an FDIC insured partner bank. BMT’s Banking-as-a-Service (“BaaS”) business model leverages partners’ existing customer bases to achieve high volume, low-cost customer acquisition in its Disbursement, White Label, and Workplace Banking businesses.

-S1 Filing

As BMT is not a bank, they are not regulated under the bank charter. Instead they are regulated under the Department of Education as they deal with US federal financial aid disbursement.

BMT consist of mainly two major operating segment.

Disbursement Business:

The disbursement business came through the acquisition of Higher One Inc in 2016.

Today, our disbursement business serves as a market leader, with disbursements of over $10 billion annually, on approximately 725 college and university campuses across the United States, consisting of over 5 million signed student enrollments (“SSEs”), representing approximately one in three eligible SSEs throughout all of the higher education institutions in the United States based on the Department of Education’s IPEDS data.

Our disbursement services provide not only revenue from fees charged to higher education institutions for those services, but also provide us with the opportunity to convert the students receiving disbursements into long-term customers of our partner bank, such that the partner bank becomes the “bank for life” for graduating and unenrolled students and services the financial needs of graduates throughout their lives, with our Company benefiting from the continued use of the BankMobile platform and through deposit servicing agreements with the partner bank.

White Label Business

White Label business started in 2019 with T-Mobile through the launch of the highly rated T-Mobile Money .

Banking as a Service (BaaS):

BMT executes the two business line through BaaS.

BMT will connect banking customers to partner banks digitally through their white-label or co-branded apps, websites, and other channels.

In return, customers have access to checking, savings, and lending products, with every feature required for customers to use the BankMobile checking account as their primary bank.

Growth:

BMT is basically using their cloud stack and someone else bank charter to help anyone launch a “bank”.

Through such a service, BMT could expect to earn

Card Revenue (interchange fees and other sources)

Deposit Servicing Fees (charged to partner banks)

Account Fees (monthly fees and certain service charges)

University Fees (dealing with a highly specialised banking function)

As long as there is more large firms trying to find ways to become more closely integrated with their customers, BMT business will grow.

Unlike the banks, white label customers (like T-mobile) aim is to build up more extensive integration with their customers to drive customer stickiness. Customers of T-Mobile would be able to do most of their banking transaction with T-Mobile money. T-Mobile will be able to better understand their customers and thus possibly create more revenue channel.

As T-Mobile Money succeeds, would the other large corporates or even the less technologically advance banks be ready to try BaaS too?

Unlike the other bank wannabe, BMT is providing the pick and shovel for the industry. No matter who finds the gold, the pick and shovel company is bound to bring in their riches.

In their latest press release, BMT indicated that they will be

Expanding their digital banking platform with customised credit monitoring and identity protection services to improve engagement and customer retention.

Marketing credit to qualified customers to drive stronger engagement and customer lifetime value.

Implementing and launching a Direct-to-Consumer segmentation strategy to provide target affinity groups with meaningful products and services.

By launching more functions, BMT could start to entrench their customers making leaving BMT platform extremely painful and difficult.

Risks:

The private label agreement with T-Mobile was just renewed for another 3 years and has an option to be renewed for another 2 years. If T-Mobile decides not to renew, we can expect a substantial drop in profit.

Higher education which forms the other bulk of BMT’s business is done through the US federal financial aid disbursement. If the US federal financial aid changes, then we could expect that business to trail off as well.

Since BMT also capitalise their R&D on software, we could expect substantial write-off if any of the scenarios above happen.

BMT has yet to shown the capability to onboard new customers other than T-Mobile.

Limited Upside:

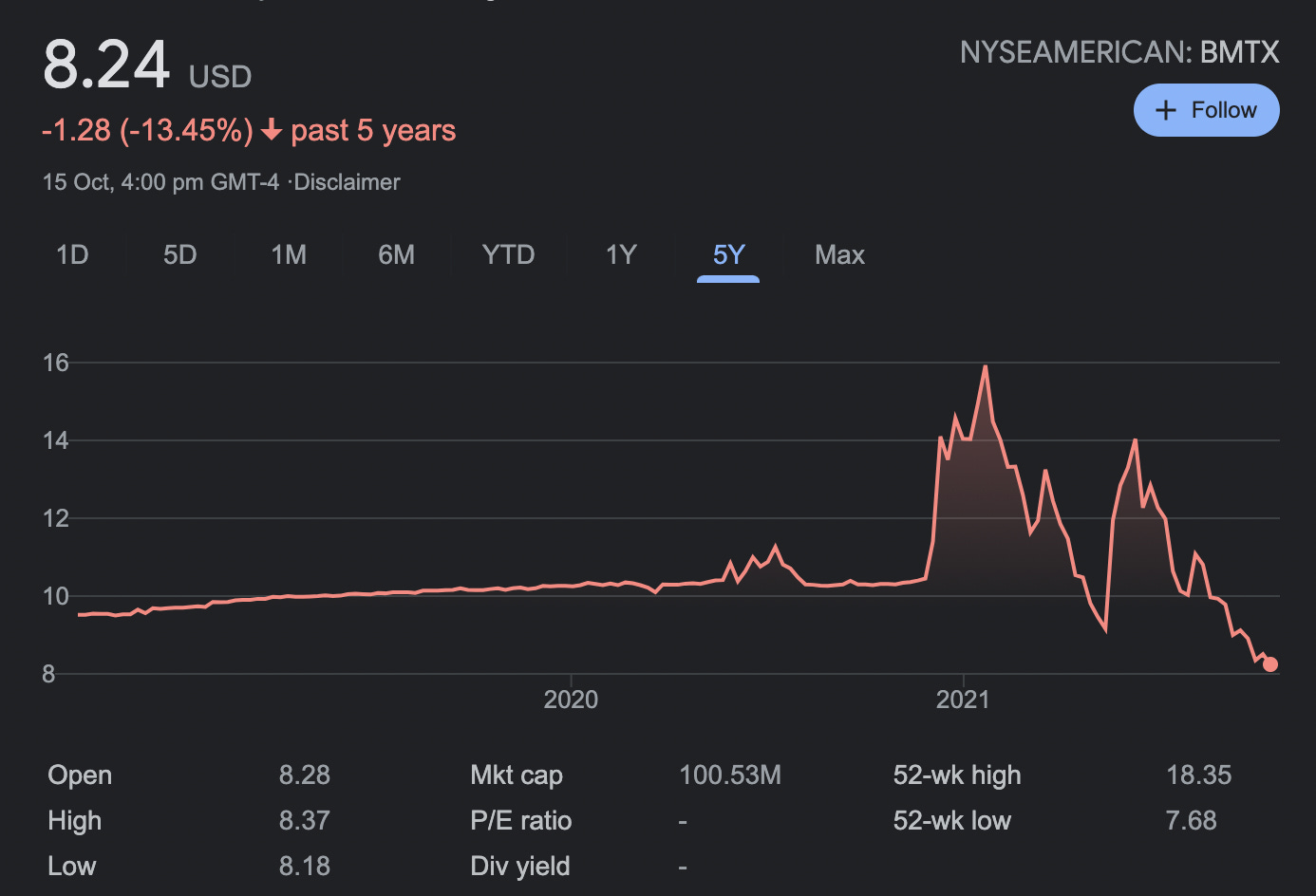

The oddest thing about a SPAC listing is that there is a potential cap on the upside. There are 12.2m shares issued but there are 23.8m outstanding warrants which could be exercised at USD 11.50.

That means that either BMT grows aggressively to justify their post warrant dilution valuation (36m shares at 11.50 = 414m) or the share price would never hit way above USD 11.50.

Limited Downside

At 12.2m shares @ USD8.24, BMT is valued at 100m.

The good thing is that it does not take a whole lot to move the needle.

At current price, and with the dilution of warrants far remove from the equation, the bet is that the ability to offer banking services (through BaaS) and entrenching your client will sound very enticing to a lot of big corporates.

It is a bet that big corporate will take to the white-label and BaaS model. Their willingness to set aside budget to try should be jingles to BMT’s ears.

Revenue would be given a nice bump with minimal cost.

The cost of adding an additional customer is like delivering the same stack given to T-Mobile Money with a change of the logo (not as simple but simple enough considering the current cloud/api tech stack). With every added customer, BMT could continue to grow their feature stack allowing for more engaged customers which should in turn drive stickiness of their customers.

In addition, BMT is currently profitable at 20212Q at tune of USD 7m with ROE of around 40%.

With some growth and a white label contract win and the share price should go no lower?

Valuation Afterthoughts:

With the current price at USD 8.00 (22nd Oct 2021), and the chance for shares to move just below USD 11.50, upside is around 43%, with an annualised yield of around 19.8% over 2 years.

If the expected improving operational numbers do not shift the share price close to USD 11.50, then the market is pricing in the dilutive warrants at this point.

That will tell me that market is indeed really forward looking…

If the BMT continue to execute and the share price continue to stuck below USD 11.50, management will most likely buy out the existing warrant holders and removing the “put option”.

and if indeed nothing really happens despite all of the above,

then I may just be the patsy here…