2021 2Q: Thoughts

Variant Perception and Sizing vs Variance and Returns

Diversification or Concentration:

Did starting the investment newsletter changed our investment style for the better?

The initial conclusion is a yes. The need to write and articulate one thoughts down also meant that there is less chance to shoot from the hip forcing me to go through the whole investment selection process.

Then the conviction/conclusion wavered.

The demand of writing a newsletter meant generating tons of new ideas on a weekly basis. That also meant a continuous need to research on new ideas rather than working on existing positions.

The need to work on breath instead on depth seems counter-productive since most of the best investors seem to be highly concentrated on their best investment ideas.

“The goal of investment is to find situations where it is safe not to diversify.” – Charlie Munger

Working on depth meant that there is a want NOT to diversify which also meant that the layer of conviction on the investment into the company has to be really high like a company which

is one which we can understand and few others do

is selling at a cheap/decent/fair valuation

has a decent forward ROE/ROIC

in a industry that is highly predictable in term of cashflow or business

is operating in an industry with more tailwind than headwind

has a ton of optionality which has a good chance of being exercised

has some form of moat within its business model where margins are protected

management are financially aligned with the shareholders

If most of the above is missing in the opportunity landscape, do I want to go for breath instead?

My idea of breath comes in the statistical strategy. That meant picking up tons of ideas which may not work for the long term.

Those in the statistical strategy may be the smaller and weaker companies, they may also be illiquid, or they may be the bigger capitalisation companies where the conviction is not strong. The assessment of probabilities of success are constantly shifting as the companies updates its strategies, publish their result and we update our understanding.

This constant updating of the prior probability distribution (prior) also lead to higher turnover of ideas as unwanted ideas are pruned and new one are added.

To accommodate this increased level of uncertainty, position sizing will be smaller.

The creation of the various strategies should technically help to navigate the risk in this market. Since the portfolio would be constantly rebalance with the best opportunities, the portfolio should weather a downturn more deftly.

The aim is that the portfolio will outperform when the market is down and will stay competitive to the market when the market is up.

Position sizing would be key to the outperformance or underperformance here.

Position Sizing:

Position sizing is a perennial issue for anyone who runs an investment portfolio for a living (even if it is a personal portfolio).

Instead of simply equal weighting every position, the aim is to combine the best world of equal weighting and dynamic weighting. Equal weight most of the smaller positions and dynamically weight the bigger positions.

That means that a few positions will weigh heavily on the result of the portfolio.

That may be the answer towards diversification and concentration.

In term of portfolio construction, the portfolio is going to keep to “10” positions.

3 concentrated position for each of the special, super and sustainable strategy and 1 large diversified “position” for the statistical strategy.

Since 75% of the portfolio comes from higher conviction, we would have the concentration to move the needle in our performance. The 25% diversification help us generate some short term returns while soaking up some spare cash while the 75% get filled.

For people who had followed the portfolio since day 1, the constant reshuffling would have irk you. The publishing of the newsletter did continuously force me to reflect and my thinking shifted on what is the most appropriate way to construct a optimal portfolio.

Variant Perception:

The construction of this portfolio also happened during the pandemic and the prevalent thought then was conservatism (just in case the pandemic turns out to be more than what what the human society could envision or handle).

The general belief that things will only get better or stocks will only get higher but hope is something I will never bank on. During the depth of the pandemic, cheap valuation are aplenty and everyone who bought anything would have been up by at least 50%.

At this moment, less so.

No. 1 was to “fish where the fish are” and No. 2 was “Don’t forget about rule No. 1.”

-Charlie Munger’s friend as mentioned in 2017 Berkshire Hathaway AGM

Investing during any market drawdown could be a variant perception. Maybe that is why all the investors become pandemic expert during the depth of the crisis.

Variant perception could be the edge in investing if it can be invalidated by subsequent information/event. The prior gets updated and the sizing changes.

But where do variant perception come from?

Variant Perception could only exist when

one can draw a hypothesis on what the market is thinking and feeling

an investment hypothesis is formulated that is different from the market

data can be collected to invalidate the hypothesis

There is simply no easy way to knowing how the whole market is thinking and feeling and thus it is often difficult to understand if the macro investment hypothesis is substantially different.

The easier way is to have a variant perception on an industry or a company. But similar to the macro forecast, the market’s view of an industry or company is often guesswork unless the company or industry is plastered all over the news outlets.

Understanding variant perception become too complicated when we need to draw on two hypothesis, 1. on the market thinking and feeling and 2. on the investment merit of the company/industry.

Two interacting hypothesis within the construct of the skull creates too much variance/possibilities for one tiny brain to handle.

A single metric that could capture both hypothesis are when expectation in the company is really low such as the market is valuing the company

so low that it is expected to fail when it is not

so low that the coming earning is bound to surprise

so low that all the optionality is price at zero

at fair value when the growth is getting bigger

at fair value when the growth is going to be going on much longer

Portfolio Expectation:

With expectation so low, the odds should be stacked in the investor’s favour.

Low expectation is one of the way to capture variant perception.

The higher the difference between the market expectation and variant perception, the higher the conviction level and the higher the possibility of higher absolute return.

When the general level of conviction is higher, we would also be having a few larger position sizing pointing towards a portfolio with higher concentration. A higher concentration will also means that the portfolio returns will have a larger variance than the market.

When the general level of conviction is lower, we would also be having more smaller position sizing pointing towards a portfolio with higher diversification. Higher diversification also means the portfolio returns will have a lower variance than the market.

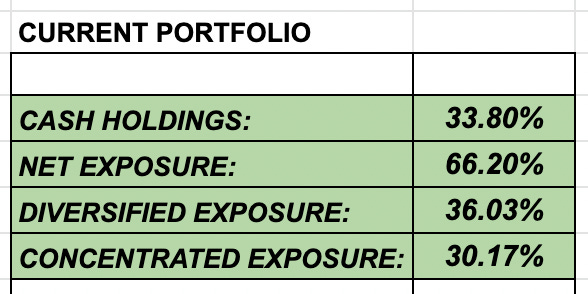

With the current market opportunity set, our portfolio looks like the below.

The portfolio is currently equally weighted across cash, diversified and concentrated portfolio.

In recent days, I had continue to add more diversified positions into the portfolio thus making sure that the source of returns are well diversified across

Different geographic region

Different industry sectors

Different time period

Different investment maturities

Different investment strategies

That also meant that absolute returns is going to slow and variance will be limited unless there is another broad based price increase in the market.

The plan and the position taken is not unlike before the crisis, we continue to be conservative and diversified until we can find conviction.

Subscribe to our newsletter if you want to receive timely information on our positions.

If you have any comments, just hit the comment button below.